Office

Office

2 & 30 International Boulevard

Modern flex-office near Canada’s largest international airport

Dave White, Head of Real Estate Debt Strategies, and Dominic Silman, Europe Head of Debt and Value-add Capital Research and Strategy, discuss how we find opportunities and the evolution of the investment landscape over the last 15 years.

Dave White and Dominic Silman discuss our investment selection process, which combines bottom-up, on-the-ground market knowledge with top-down, macroeconomic and geopolitical analysis to identify attractive investments that meet our investment criteria.

In addition to how we identify opportunities, they cover where we are likely to invest, and how the opportunities before us have evolved over the last decade and a half.

Want to read more?

Dave White, Head of Real Estate Debt Strategies, and Brett Ormrod, Net Zero Carbon Lead for Europe, discuss the current and future state of green lending across Europe.

While lending volumes across the market remain volatile, data shows one continuously increasing metric: the demand for green loans, which is being driven by the ever-growing sustainability requirements from both investors and sponsors.

Dave White and Brett Ormrod discuss the challenges that borrowers and investors are facing, and how we at LaSalle are navigating these dynamics. They discuss how green loans are impacting the European real estate market, what they can mean for investors’ bottom lines, and the overall opportunity not just for green loans, but for greener assets in investors’ portfolios.

Want to read more?

A prudent person sees trouble coming and ducks.

A simpleton walks in blindly and is clobbered.

— Proverbs 22:3

King Solomon’s words of wisdom have been passed down to us for 3,000 years. They still resonate, especially in this modern translation,1 even though the “trouble” is no longer invading Assyrians or Babylonians but the type of danger we bring on ourselves through an all-too-human combination of ingenuity, hubris and ignorance.

Watch any movie from the 1930s to the 1960s and you will see actors inhaling tobacco smoke with abandon. We know better now. Like the generational awareness of the harm caused by tobacco products, real estate owners have gradually become aware of the dangers lurking in certain building materials and contaminated soil. Starting in the 1960s, societies have spent fortunes cleaning up “miracle products.” Asbestos, PCBs, dry cleaning solvents, herbicides and lead pipes were all considered state-of-the-art technologies at various points in human history. None of these inventions were designed with the intention of killing people. They all started with a noble purpose – whether suppressing catastrophic fires, insulating transformers, cleaning wool suits or producing a pleasing nicotine buzz that also curbed the appetite. The “externalities” associated with societal damage from the use of these products took decades to discover and billions to eradicate.

Greenhouse gas emissions share a common ancestry with these miracle products. Heating buildings with diesel fuels, running gas lines through city streets, producing electricity with coal-fired plants—these were all logical, economical, and sensible solutions to the problem of bringing energy to homes, businesses and buildings of all types. The industrial revolution accelerated the growth of cities and raised the quality of life for millions of people by dragging them out of rural poverty. As we now know, society’s dependence on fossil fuels creates new problems which must be dealt with.

The recognition that miracle products can carry hidden (or not so hidden) dangers follows a predictable pattern. Here is what the step-by-step process often looks like:

Evidence and awareness. An environmental problem often requires decades of scientific study and mountains of evidence to convince people that a change is necessary. Even as this evidence accumulates, vested interests organize counterattacks to convince society that the problem is non-existent or over-stated. Eventually the harm to human life becomes so obvious that denial becomes a “fringe position.”

Market demand. In many cases, the process of partial “market adjustment” can begin ahead of government action. Voluntary data collection and industry-led reforms start the slow process of change. In the case of greenhouse gases, the marginal contribution of each emitter is so small, and so embedded in society, that government interventions sometimes lag market-led shifts (e.g., the adoption of LED lighting or heat pumps).

Regulatory response. Yet, government interventions are almost always needed to accelerate and complete behavioral change to truly eliminate harm to the environment and to human life created by “externalities.” These regulations and policy responses often get pushback as competing outcomes are debated in the political arena. Economists agree that putting a price on carbon would be the most efficient and effective solution, but a market mechanism for carbon pricing requires government intervention — in the form of a carbon “tax” or to set up an emissions trading scheme.

Benchmarks and best practices. Eventually, the rise of data benchmarks and peer group comparisons begins to shed light on who, where and how successful “treatments” are applied to any environmental problem. Engineering and laboratory science helps inform this stage of the process, as does public health or industry group data. Integration with market investment processes and decisions leads to a focus on reversing years of damage to the environment and compliance with new regulations and guidelines. At this stage, market-driven and regulatory-driven changes start to converge.

Price integration. Feedback loops are established where type 1 errors (false positives) and type 2 errors (false negative—or overlooked problems) are exposed.2 In loosely regulated situations like climate change, the efficient market hypothesis (EMH) takes hold as the change process gets partially or fully priced by consumers and producers. Economists and policy analysts favor the practice of placing a “price” on an externality to compensate society for the harm. In practice, though, compensatory payments to offset environmental damage are often decided through the courts and litigation.

Continued market and regulatory evolution. The enforcement of tighter regulations also follows its own trajectory depending on the governance structure of a particular country or urban jurisdiction and the toxicity of the problem. The discipline of epidemiology, using population data and public health analysis, is especially helpful at this stage of refining the policy solutions.

The Transition from “Data” to “Wisdom”

For the de-carbonization of buildings, various markets and countries are well into Step 3 (Regulatory Response) and Step 4 (Benchmarks and Best Practices). In Europe the “theory of change” is focused more on EU-wide or national policies to promote energy disclosures through top-down regulatory solutions. In the United States, the emphasis is based more on voluntary pledges, market solutions and regulations that are based on specific local jurisdictions. In most developed countries, steps 5 (Price Integration) and 6 (Market and Regulatory Evolution) are underway, but both have a long way to go.

The rise of real estate sustainability benchmarks (like GRESB) has accelerated in recent years. In many cases, they have expanded to include social factors and tenant well-being alongside environmental metrics. The next hurdle, though, is to establish materiality tests that infuse meaning, and determine financial impacts based on the volumes of reporting that the industry has started to produce and disclose.

Reading through ESG reports often reveals the triumph of reporting and public relations over salience or relevance. The conjoint challenges of reducing building emissions alongside improving the well-being of building users and the surrounding communities can be obscured by data denominated in less familiar metrics like tons of CO2 or Kilowatt hours. In time, and with experience, the emphasis will shift to what truly moves the needle on all elements of the “sustainable investing” paradigm—and which metrics give off misleading or meaningless “virtue” signals.

Financial metrics align most closely with the “fiduciary duty” of an investor. Moreover, stakeholders have decades of experience analyzing and interpreting financial data. It will take additional time and effort to convert environmental data into financial terms or to simply raise the consciousness of how to interpret energy and emission data in its own right. (LaSalle’s work on the “Value of Green” synthesizes studies of the evidence linking sustainability metrics and financial outcomes. An update on this work is below.)

In writing Proverbs, King Solomon gathered centuries of wisdom based on experience. In the modern world, we often believe that the steps to wisdom are built on a foundation of knowledge, information, and data. The famous “DIKW” hierarchy has been a mainstay of information sciences since the 1930s. Sustainability wisdom is still in the process of being formulated and likely requires more time to make progress. Fortunately, the foundations of this wisdom are already being put in place—first through data (the modern way to refer to many, many experiences), then information (organized and analyzed data), eventually leading to knowledge (patterns are identified and the “what” and “why” questions are answered) and finally reaching the status of accumulated wisdom (how to respond). This is a path that humans have traveled before. More lives are at stake this time around and the wisdom may not be easily agreed upon by all industries, countries and stakeholders. Nevertheless, the search for sustainability wisdom must continue and time is of the essence.

Revisiting LaSalle’s “Value of Green”

In September 2023, LaSalle published our ISA Focus report What is the value of green? Looking at the evidence linking sustainability and real estate outcomes. The report presents a framework on how sustainable attributes of properties can be viewed as both as drivers and protectors of value, along with showcasing findings from the broader literature. We continue to maintain a Value of Green tracker, monitoring research on this subject as it is produced. Some of the findings that have surfaced since the release of our initial report are worth highlighting:

Beyond the direct links between sustainability and historical investment performance in terms of return, rent and value premiums, more signals are emerging as available data on the topic grows, and becomes increasingly forward looking:

Beyond results based on backward-looking data, detailed case studies of investments into sustainable initiatives are being published. The JLL report “Future-Proof Your Investments“ showcased opportunities for sustainable New York offices; another example is CBRE’s report “The impact of on-site rooftop solar on logistics property values.”

Tobias Lindqvist

Strategist, Climate and Carbon Lead, London

Sources:

CBRE (March 2024) UK Sustainability Index Results to Q4 2023. CBRE

P. Torres, G. Bolino, P. Stepan (2024) The Green Tipping Point. JLL

T.Leahy (2022) London and Paris Offices: Green Premium Emerges. MSCI

P. Torres, J. del Alamo (July 2024) Future-proof your investments. JLL

D. Marina, J. Tromp, T. Vezyridis, O. Bruusgaard (July 2023) The impact of on-site rooftop solar PV on logistics property values. CBRE

O. Muir, Y. Chen, T. Metcalf et.al (Dec 2023) Green premium: Study of New York and London Real Estate finds strong evidence for a ‘green premium’. UBS

What can we learn from simulations?

The de-carbonization of buildings is taking place in a complex and ever-changing environment. It is a multi-dimensional problem replete with uncertain outcomes, regulatory change, shifting societal norms and markets, and the politicization of sensitive issues.

At the June 2024 MIT World Real Estate Forum, Professor Roberto Rigobon unveiled a “sustainability simulation” game patterned on his pathbreaking work on social preferences for the European Commission. The technique shows how the traditional economic conceit that we make “resource trade-offs” does not accurately capture how humans make decisions when faced with multi-dimensional choices.

In the simulation, the audience was given nine choices for different retrofit projects for a commercial building. Each choice resulted in simultaneous movement across three metrics that the audience had already established that they cared about — changes in NOI (profitability), CO2 emissions, and tenant satisfaction/well-being. The cost of the projects was amortized into the NOI calculations and the other metrics were also calibrated based on actual data from the US.

The simulation showed that a knowledgeable real estate audience rarely solves just for “pure profits” at the expense of tenant well-being or CO2 emissions. The simulation also mimicked reality—where sometimes profitability moves in synch with reduced CO2 emissions and other times it moves it moves in the opposite direction. The simulation was designed to show how the co-movement depends on the local market and the type of de-carbonization project. Tenant well-being and CO2 emissions could be implicitly linked to revenue when and if participants believe that occupancy, rents and capital raising are all interconnected.

Through their choices, the audience tried to optimize across all three priorities at once — leading to an interesting result that revealed their average willingness to “pay” to reduce a ton of CO2 emissions of about $200 ton. Yet, if asked directly how much they would pay to reduce a ton of greenhouse gas coming from a building, it seems unlikely that many would have volunteered to pay that much. This finding also shows how the language of profitability and returns is much more advanced than the metrics and concepts associated with either decarbonization or tenant satisfaction. And that all these metrics are linked, but not fully integrated in the minds of real estate professionals.

Only a few participants in the game focused only on reducing CO2 (at the expense of decent profits). And just a few focused exclusively on profitability at the expense of tenant satisfaction or CO2 emissions. This seems like a reasonable facsimile of what enlightened investors will do — especially when they know that their actions are being disclosed. As we learn more from these simulations, it is possible that policy makers will be able to refine the mix of incentives and regulations that govern the real estate industry.

Jacques Gordon

Cambridge, Massachusetts

LOOKING AHEAD >

Footnotes

1 The Message, translated from the Hebrew scriptures by Eugene Peterson (1993-2002).

2 These are all part of the learning that occurs with any “treatment hypothesis.” The science of public health provides solid evidence to weigh whether the “treatment” is helping, hurting or having no impact on the eradication of the underlying disease. In real estate, a good example of this is the gradual discovery that with certain types of asbestos, it is more dangerous to remove it than to “encapsulate” it in an existing structure. The science of “decarbonization” is still being established to determine whether, for example, the mass production of lithium batteries does as much harm as the burning of fossil fuels. For real estate and climate change, the “treatment” will likely focus on energy efficiency/ decarbonization interventions that are a combination of government penalties/incentives and voluntary actions. The effectiveness of these treatments will depend on compliance, market response, and how well interventions find acceptance through the political process.

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

This article first appeared in the August 2024 edition of IPE Real Assets

With increasing regulations and more investors embedding sustainability goals into their investments, incorporating green targets into the debt component of the capital structure is becoming more common. As a result, the debt market across Europe is becoming a two-tiered market, with more green loans being issued at the same time as overall lending volumes have declined.

In this guest article for IPE Real Assets, Dave White discussed the growing appetite for these loans across Europe, and how both lenders and investors are responding to this changing landscape.

At LaSalle, we are often asked what investors in real estate debt and what borrowers of our credit solutions can expect from us.

For investors, knowing that their investment manager has successful, long-term relationships with their borrowers is a strong sign that those interactions will continue, and that attractive investment opportunities will remain available. This dynamic allows us to remain both disciplined and selective in the areas where we choose to invest capital.

For borrowers, recognizing that their credit provider has a wide range of capital solutions, and can offer competitive terms backed by certainty of execution is paramount to our success. Further, this is what drives such a high repeat borrower base and the ability to foster long-term relationships with our borrowers.

As one of the largest providers alterative credit solutions in Europe1, we find ourselves in the enviable position of being able to truly understand how important both borrowers and investors are to the whole equation. This dynamic allows us to remain active investors in this market, highlighting our expertise in the sector.

What can real estate debt investors expect from LaSalle?

What can real estate debt borrowers expect from LaSalle?

Want to read more?

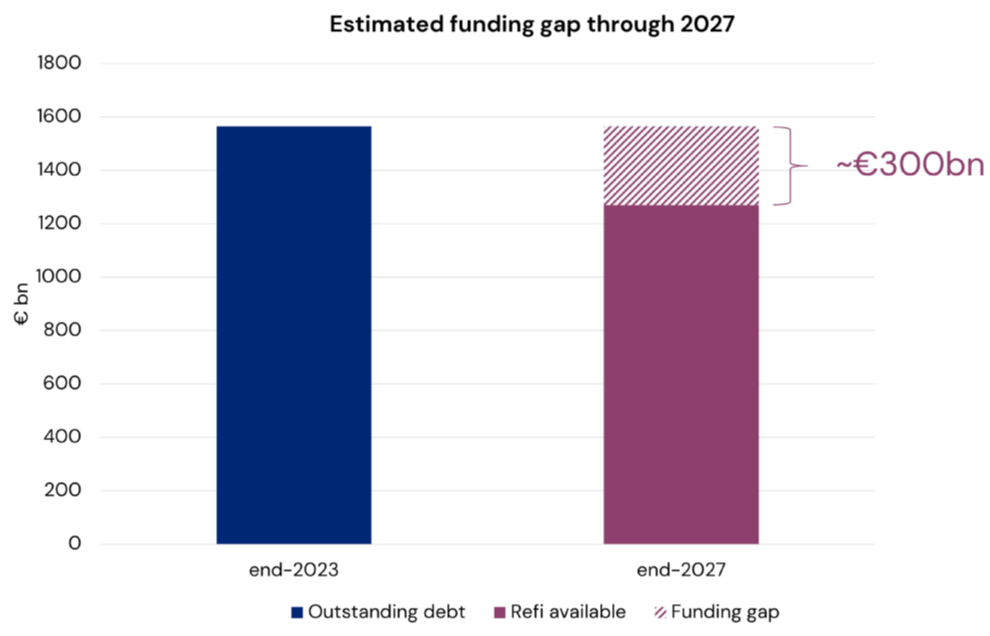

While traditional banks’ appetite for providing commercial real estate loans has declined, other lenders (including investment management firms such as LaSalle) have moved in to fill the funding gap. As a result, we have recently seen increasing interest from institutional investors in real estate debt.

But what is it about real estate debt that makes it a compelling investment? As the second largest of the “four quadrants” of real estate, it has a value in the US and Europe alone of approximately US $4.5 trillion, representing an enormous opportunity. Real estate debt historically has produced competitive risk-adjusted returns in addition to showing low correlation to other assets.

In our latest research, we examine the three-part case for investment, including:

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

LaSalle is one of Europe’s largest and most established investors in real estate debt, offering a variety of loan types across sectors. Learn more about this dynamic asset class, and LaSalle’s capabilities from Dave White, Head of European Debt Strategies here at LaSalle.

Want to read more?

Dave White, Head of Real Estate Debt Strategies, Europe discusses the market in 2024 and where we are seeing opportunities for investors.

Want to read more?

“You take the blue pill—the story ends, you wake up in your bed and believe whatever you want to believe. You take the red pill… all I’m offering is the truth.”

– Morpheus to Neo, The Matrix (1999)

We published the global chapter of the ISA Outlook 2024 on November 14, 2023, just before euphoria about a potential ‘V’-shaped property market turnaround emerged. Interest rates fell quickly as financial markets priced in several US Federal Reserve (Fed) rate cuts in 2024. For a time, it looked as though our prediction that it would take a little longer for markets to digest a renewed spike in rates would not age well.

In this Mid-Year Update, however, we look back to find an outlook with an uncanny resemblance to that of six months ago. This is not because nothing has changed, but because the mood has gone full circle. The landscape remains characterized by interest rate volatility, soft fundamentals in some markets, and gaping quality divides, but also by pockets of considerable strength. Another factor that has not changed is that financial conditions (i.e., interest rates) remain the dominant driver of the market, and that political and geopolitical uncertainties are in focus in many countries (see LaSalle Macro Quarterly, or LMQ, pages 4-6).1

In this report, we discuss five themes we see driving real estate markets for the rest of 2024 and beyond. At our European Investor Summit in May, our colleague Dan Mahoney argued that—like Neo in the Matrix—we should take the red pill and endeavor to see the market as it is, not as we’d like it to be. Taking the red pill requires a realistic view on property values. It reveals as unlikely a return to an environment of ultra-low interest rates or uniformly benign fundamentals in the “winning” sectors.

But it does not mean that there will not be attractive investment opportunities. Unlike the bleak dystopia of The Matrix, there are many reasons for optimism, as well as signs that the coming months will come to be seen as a favorable investment vintage. That said, investing successfully will require a balance of big-picture perspective and granular discernment, and a mix of patience and willingness to take risk.

Over the past year, we likened the interest rate path in most markets to a strenuous mountain trek: the relentless climb (2022), the range-bound altitude of an alpine ridge line (H1 2023), the unexpected upward turn in the trail (Q3 2023), and the mountain meadow of cooling inflation and expected rate cuts (Q1 2024). More recently, there have been upward turns in the interest rates trail whenever there have been signs of sticky inflation in the US and other key countries.

One thing is for sure: No map exists for this trail. While interest rates have big consequences for real estate capital markets, they are extremely difficult to predict. We continue to caution investors against overconfidence in their ability to forecast the path of long-term interest rates.

Mercifully, falling rates are not a necessary condition for a robust recovery in real estate transaction activity. Despite interest rates remaining elevated, property markets are already showing signs of finding their footing, such as renewed US CMBS issuance and resilient deal volumes in many markets and sectors.2 A key reason for this is that wherever interest rates have spiked over the past two and half years, especially Europe and North America,3 real estate prices have by now adjusted downward significantly. The relativities between expected returns for real estate and those for other asset classes now look more appropriate than they have in many months; in other words, more of the market is at or near fair value.4

That said, while lower rates are not necessary for real estate capital market normalization, greater stability in rates than we have been seeing would no doubt help. Interest rate volatility is the enemy of a smoothly functioning private real estate transaction market. Excessive movement in borrowing costs during due diligence periods can lead to dropped deals and re-trades. Moreover, when rates are volatile, the conclusions of fair value models are also volatile, impacting both buyers’ and sellers’ assessments of appropriate pricing. Looking at recent trends in the MOVE index,5,6 interest rate volatility appears to be gradually easing but is still elevated relative to recent history (see LMQ page 13).

Increasing stability in rates is welcome, but for now it is reasonable to expect continued strains in real estate capital markets that create both challenges and opportunities. Such conditions can represent favorable entry points for debt investors (lenders), distressed equity players and core investors seeking entry points below replacement

Over the past half-year, interest rates have been increasingly influenced by widening divergences between near-term growth, inflation and monetary and fiscal policy outlooks. Most notably, the bond yield gap between the US and other markets, especially the eurozone, has widened. US growth and inflation have surprised on the upside, in the face of softening or stability elsewhere. Markets currently expect only one Fed rate cut in 2024, down from up to four earlier in the year.7 Meanwhile, in early June the Bank of Canada became the first G7 central bank to cut rates since the great tightening cycle began, with the European Central Bank (ECB) following shortly after (see LMQ page 7).

Regional groupings can obscure divergences within them. The key driver of eurozone softness is Germany (see LMQ page 23), owing to its reliance on manufacturing exports and past dependance on Russian energy. Meanwhile, the Spanish economy remains strong due to healthy consumption and tourism. Within North America, Canada’s economy is underperforming the US because the structure of its residential mortgage market makes it more exposed to higher rates.8 These intra-regional variations may have a range of impacts on property markets, for example by shifting the relative short-term prospects for demand and value.

Japan and China represent long-standing divergences that persist.9 In China, a loosening bias remains in effect as inflation hovers at around 0%.10 In Japan, monetary policy is gradually normalizing, but so far without triggering a big increase in interest rates (at least compared to elsewhere). In March, the Bank of Japan (BOJ) abandoned negative interest rates and ended most unorthodox monetary policies, though it has since held policy interest rates at around zero. Japan’s economy becoming more “normal” is generally a positive, but interest rate differentials have pushed the yen to a 34-year low against the US dollar (see LMQ page 14), creating upside risks to inflation.11 But notably, Japan remains the one major global market in which real estate leverage remains broadly accretive to going-in yields.

Aside from reinforcing the potential benefits of diversification, what do these divergences mean for investors? Mechanically, any unexpected relative softening of interest rates should, all else equal, be beneficial for relative value assessments of real estate in that market. But firmer rates in the US have predictably come alongside a stronger US dollar. This points to practical limits to global monetary policy divergences; central bankers are keenly aware that weaker currencies come with inflationary risks. Moreover, it is worth asking how persistent macro divergences will be; current divergences are rooted in timing differences of expected rate cuts, rather than an anticipated permanent disconnect.

For several years, secular themes and structural shocks have dominated the trajectories of global property markets. But there is a clear cyclical pattern reemerging in the form of a pronounced upswing in vacancy across global logistics markets, and in US apartments. The return of cyclicality in those favored sectors is having significant impacts on their near-term prospects.

The softening trend is not new. In the ISA Outlook 2024, we identified hot sectors “coming off the boil.” Part of this was down to normalizing demand levels, but elevated new supply was also a key driver. As expected, the softening we observed has continued to deepen, leading to outright rent declines in certain markets, especially for apartments in US sunbelt metros.

Softening fundamentals are not to be ignored, but we recommend investors to have the conviction to “ride the wave” of excess supply. Wide variation in supply levels at the market and submarket level means that investors with granular market data and the discipline to incorporate it into their market targeting processes should be positioned to select the most attractive markets and submarkets.

Moreover, the forces that create cycles sow the seeds of their own reversal; we expect the current supply wave to moderate soon, as evidenced by sharply falling construction starts (see LMQ page 25). Many of the projects being completed today broke ground when credible exit cap rate assumptions were several hundred basis points lower than today. Higher interest rates upended development economics; far fewer new developments can now be justified on today’s mix of land prices, construction costs and financial conditions.

Finally, investors should be prepared to think about cash flows in both real and nominal terms. When cooling nominal rental growth comes alongside cooling inflation, as it does today, it is possible for that to be consistent with solid real rental growth, depending on the relative magnitude of each.

Beyond the reassertion of supply cycles in some markets, there is an evolving mix of secular stories that deserve attention. Some of these are so long-standing that they could almost be considered constants. These include structural shortages of housing in most of Europe, Canada and Australia, as well as the widespread changing definition of core real estate in favor of more operational niche sectors and sub-types.12 We continue to be strong advocates for investment in undersupplied living sectors, and for participating in the institutionalization and growth of niche sub-sectors such as single-family rental (SFR) and industrial outdoor storage (IOS).

More dynamic themes that deserve a closer look include the stabilization of retail real estate and divergent office investment prospects:

Other key secular themes driving investment opportunities today include the implications of artificial intelligence (AI) adoption for data center demand, student mobility for student accommodation in Europe and Australia and aging for senior housing.

Past experience of real estate cycles suggests that the best investment opportunities tend to arise in periods marked by significant uncertainty, volatility and pessimism, but also when early signs of improvement and stabilization are present—in other words, moments similar to today’s environment. Experience also reinforces that it is nearly impossible to time the market, so it is best to be selectively active throughout the cycle. By the time the “all clear” signal is sounded after a market crisis, it is too late to achieve the best risk-adjusted returns.

That said, “red pill” thinking means we must recognize that the coming capital market rebound is unlikely to be as sharp as it was after the Global Financial Crisis (GFC), given that central banks are unlikely to usher in ultra-loose policy. Seeing the market as it is requires accepting the likelihood that interest rates could remain sticky, and a realistic view of near-term fundamentals as a wave of supply impacts some sectors.

Footnotes

1 Also see our ISA Briefing, “Elections everywhere, all at once: Geopolitics and risk”, April 2024. In that note, we highlighted the various sources of political uncertainty this year and outlined how we recommend investors consider these risks. At the time of writing, political developments are particularly salient for short-term movements markets in France and the UK, given elections that have been called in those countries.

2 Source: MSCI Real Capital Analytics and Trepp

3 Japan and China are key exceptions that we cover in greater depth under the “deciphering divergence” header.

4 Of course, there is considerable variation embedded in this and any assessment of fair value. As always, the devil is in the detail on the assumptions that go into expected and required returns; at LaSalle, specific fair value inputs and conclusions remain a proprietary output.

5 The Merrill Lynch Option Volatility Estimate (MOVE) is a market-implied measure of volatility in the market for US Treasuries. It calculates options prices to reflect the expectations of market participants on future volatility. Observation made as of June 24, 2024.

6 Source: Bloomberg as of June 26, 2024.

7 For more discussion of the Canada-US divergence and the consequences of mortgage rate resets, see our ISA Briefing, ”The impact of residential mortgage resets”.

8 For more detailed discussion of the unique factors in the Japanese and Chinese macro environment, see our ISA Briefing, “Key economic questions for China and Japan”.

9 Source: Oxford Economics; Gavekal Dragonomics as of June 26, 2024.

10 Economic theory suggest that weak currency may contribute to inflationary forces because it pushes up the cost of imported goods.

11 See our PREA Quarterly article on “The Changing Definition of Core Real Estate” for a discussion of how the characteristics considered desirable in core properties is moving from traditional metrics like lease length, to observed qualities like the stability of cash flows. This shift elevates the appeal of niche sectors sub-sectors versus traditional sectors such as conventional office.

12 See our ISA Focus report “Revisiting the future of office”, published March 2023.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

This article first appeared in the June 2024 edition of PERE

LaSalle’s Dan Mahoney sat down with peers from across the industry to discuss the state of the UK real estate market.

UK real estate’s rocky road to recovery

After a period of political and economic turbulence, not to mention real estate market paralysis, participants in PERE’s UK roundtable anticipate calmer waters ahead, writes Stuart Watson

For the participants in this year’s PERE UK roundtable discussion, certainty is a welcome thing, following as it does a prolonged period of political turbulence that saw the UK withdraw from the European Union, combined with both the covid-19 pandemic and the global supply chain and inflation shocks that disrupted the UK real estate investment market.

Want to read more?

Over the last several years, we have seen an increase in the number of institutional investors around the world interested in adding real estate debt to their portfolios.1 In some instances, this is to replace an allocation to traditional fixed income, while in others it is both an enhancement and a way to further diversify their current level of real estate holdings.

Real estate debt versus traditional fixed income

Real estate debt differs from traditional fixed income investments in a variety of ways, primarily through collateralization, income generation, differing risk factors, the potential for securitization and its direct relationship to underlying real estate assets. In the same way that investors looking for reliable income streams and relative stability across a number of fixed income products such as government bonds or corporate credit, they can also turn to real estate debt investments.

One key differentiator for the asset class is that it is typically secured by tangible collateral in the form of real estate. Further, real estate credit investments benefit from attractive positions within a capital structure, benefitting from a subordinated first-loss position from equity, and also from negative control structures which give lenders an ability to proactively protect capital in a downside scenario. In contrast, traditional fixed income investments such as corporate or government bonds are usually unsecured and rely solely on the creditworthiness of the issuer.

For many institutional investors, income generation is a key objective and something that real estate debt investments can generate primarily through interest payments on the loan. These interest payments are often higher than on traditional fixed income investments such as sovereign or investment-grade corporate bonds. Additionally, real estate debt may also offer the potential for additional income through loan origination and exit fees, or in some instances, profit participation. Like other investments in any asset class, real estate assets are subject to market fluctuations and economic cycles. There are, however, additional property-specific risks that investors should take into consideration. These include factors such as underlying occupancy and cash-flow drivers as well as capital markets. Investors should also consider the wider macroeconomic and credit-risk considerations that investors in listed fixed income must factor into their decision making. Lending against property embeds the possibility of active takeovers, also known as workouts, requiring hands-on asset management expertise.

In some instances, real estate debt can be securitized, meaning loans are packaged together and sold as securities in the market. This allows investors to gain exposure to real estate debt through mortgage-backed securities (MBS) or collateralized debt obligations (CDOs). Traditional fixed income investments, on the other hand, are typically traded as individual bonds or included in bond funds.

Lastly, real estate debt investments are directly tied to specific properties or real estate platforms. The performance of the underlying property and its cash flows can impact the value of the debt, along with a borrower’s ability to repay it. Traditional fixed income investments are generally linked to the creditworthiness and financial health of the issuer, without a direct connection to specific underlying assets.

So why should institutional investors consider real estate debt?

As with any other asset class, real estate debt has its own unique set of attributes which, as part of a diversified, risk-adjusted portfolio, may provide investors with compelling reasons to include it within their overall strategy.

Key benefits may include:

As always, it’s important that real estate debt, like any other asset class, is considered as a component part of an overall portfolio of investments constructed with the underlying objectives of the investor in mind. When properly integrated into a portfolio, real estate debt investments have the potential to offer institutional investors the opportunity to generate stable income, diversify their portfolios, align their investments with long-term liabilities, protect against inflation, target attractive risk-adjusted returns and, in some cases, adhere to regulatory requirements.

Understanding the capital structure

The term “capital structure” in real estate investment is used to represent layers of debt and equity within an investment structure, each with its own risk-return profile and repayment priority. Investors choose a position in the structure based on risk appetite, desired returns and level of control or ownership in the investment. LaSalle invests across all layers of the capital structure.

Common equity represents an ownership stake of the property. These investors bear the highest risk but also have the potential for the highest returns. They participate in the property’s cash flows and profit distributions only after others have been paid. They have the greatest exposure to the property’s performance and value appreciation but also face the greatest risk during market downturns or property underperformance.

Preferred equity represents a hybrid investment between debt and equity. These investors provide capital to the project but have a higher claim on profits and cash flows than common equity holders. They enjoy a priority in distribution but still hold a subordinate position to debt holders. They often receive a fixed return, similar to interest on debt, and may also have upside potential linked to a property’s appreciation in value.

Mezzanine debt sits between senior debt and equity in the capital structure. Mezzanine lenders provide loans that have secondary priority in terms of repayment but carry a higher risk profile compared to senior debt. As a result, they tend to offer higher interest rates or additional equity-like features to compensate for the increased risk.

Senior debt occupies the most senior position in the capital structure and has the highest priority for repayment in case of default or enforcement. Lenders providing senior loans hold the first lien on the property, meaning they have the first claim to cash flows and proceeds in the event of liquidation and are usually secured by asset level security. Typically, senior debt offers lower yields compared to other subordinated positions within the capital structure due to its lower risk profile.

1 INREV Investment Intentions Survey, 2017 – 2024

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment. LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance. By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management. GL001731MAY25

This article first appeared in the May 2024 edition of PERE

LaSalle’s Dave White sat down with peers from other leading alternative credit providers across Europe to discuss the state of real estate debt across the continent.

Opportunities are slow to unfold in European real estate debt

A golden era for alternative real estate lenders has so far failed to get underway. But there are signs the machinery is becoming unclogged, writes Judi Seebus

A year ago, alternative real estate lenders in Europe were convinced they were on the cusp of a golden age. During PERE’s European debt roundtable discussion in March 2023, participants spoke of a “huge” opportunity ahead to take advantage of a potential shortfall in refinancing funds for maturing loans amid a potential retrenchment from traditional lending sources. “I have seldom been this excited to be investing in debt,” said one participant.

Want to read more?

Report Summary: Physical climate risk data can be a powerful tool for managing asset and portfolio risk and returns. Learn what strategies leading firms are using to manage physical climate risks and navigate market challenges. The latest report from the Urban Land Institute and LaSalle Investment Management builds on their previous report, How to Choose, Use, and Better Understand Climate Risk Analytics, to describe how leading firms are leveraging physical climate-risk data in underwriting practices. With insight into asset- and portfolio-level risk becoming increasingly easy to obtain, new challenges lie in effective interpretation and integration of information into investment practices. Relying on research and interviews with industry leaders, this report provides a nuanced exploration of this emergent issue.

Physical Climate Risks and Underwriting Practices in Assets and Portfolios is structured into three sections, each addressing different aspects of the industry’s response to climate-risk data:

Section 1. Explore the current state of the industry, finding that:

• Leading firms actively coach their teams on physical risk.

• Regulatory trends affect, but do not motivate physical risk assessment.

• Different geographies approach physical with their own level of urgency.

• Investment managers tend to focus on fund risk, capital providers on portfolio risk.

• Tools to understand and price physical risk are still in a nascent stage of development.

Section 2. Examines the application of climate data in decision making. Key findings include:

• Aggregate physical risk is a screening tool; individual hazard risk is actionable information.

• Climate value at risk remains opaque; the utility of the single number offers value but needs increased transparency.

• Atypical hazard risk (e.g., flood in a desert) merits increased attention.

• External consultants can frequently fill skill gaps, especially for firms with less in-house expertise.

• While no predominant timeframe or Representative Concentration Pathway (RCP) emerged as industry standard, the 2030 and 2050 benchmarks were the most commonly referenced time horizon.

Section 3. Assess the impact of physical climate risk on acquisition, underwriting, and disposition practices; finding that:

• Leading firms start with a top-down assessment of physical risk.

• Market concentration of physical risk is analogous to other concentration risks—a nuanced analysis is required.

• Capital expenditure for resilience projections is a key forecast but rife with uncertainty.

• Local-market climate mitigation measures are important to understand but difficult to forecast.

• Exit cap rate discount for estimated physical risk is an increasingly commonly used tool, frequently 25 to 50 basis points.

• Firms infrequently disclose physical risk but the market needs increased transparency.

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

Roughly 60% of the world’s population lives in countries facing major elections in 2024, markets representing 65% of the institutional investable real estate universe.1 Elections are, of course, the cornerstone of the democratic process, which in turn underpins the appeal of the most transparent, investable markets; that said, elections come with the possibility of policy changes that may impact returns. Today’s geopolitical risks, whether they be this continuing election super-cycle (see LaSalle Macro Quarterly, or LMQ, page 4), or the various ongoing conflicts and trade disruptions, prompt important questions about how to manage investment risks related to these themes.

One of the protagonists in the Oscar-winning film Everything Everywhere All at Once says that being “’right’ is a small box invented by people who are afraid.” LaSalle’s risk management philosophy emphasizes optimizing risk/return trade-offs rather than minimizing risk-taking, while recognizing the limitations of point-estimate predictions and base-case scenarios — that is, attempts at “being right.” Today’s geopolitical events are especially likely to confound any forecaster seeking to be exactly right.

How should an investor manage their assets in the context of “unknowables” about which engaging in guesswork is tempting, but being “right” is elusive? What frameworks do we have to mitigate geopolitical risks? We propose six recommendations to keep in mind for investors taking stock of the many elections, and several conflicts, that may impact markets in 2024.

There are many examples of ex ante predictions of elections’ investment implications having been overstated. For instance, leading up to the 2016 US presidential election, there were widespread predictions that the US economy would be significantly negatively impacted by Donald Trump’s anti-immigration and protectionist stance were he elected.2 In the event, equity markets rebounded strongly after a short-lived hit and the US economy proved resilient to the changes in rhetoric and policy that came with a new president.3

Looking ahead to the US elections later this year, almost certainly a rematch between Biden and Trump, coverage of the candidates’ differences should be accompanied by awareness of their similarities. Both candidates seek to prioritize domestic production, which could lead to greater levels of on- or near-shoring of supply chains.4 Moreover, election prediction odds (see LMQ page 6) suggest divided control of the two houses of Congress and the presidency is likely; divided government has typically been associated with relative stability in domestic policy, which is generally positive for markets.5 Both of these factors — at least in isolation — point to the potential for news cycle hype to overstate long-term market impacts of this particular election.

Financial theory tells us that systematic risks are undiversifiable.6 Systematic factors are those with significant, far-reaching implications that affect the price of all assets. But financial theory also entertains that different assets may have different sensitivities to the same set of factors; an asset’s “beta” signifies the responsiveness of its price to a given factor. This is a useful way to think about an investment’s sensitivity to political and geopolitical events. For example, a property in a metro area whose economy is heavily driven by government spending would likely have a high sensitivity to political changes. Another example could be that a property located in the Baltic States, ex-Soviet countries on the border with Russia, is likely to be especially sensitive to developments concerning relations between Russia and the West. Investors should be mindful of assets’ expected sensitivities to geopolitics, whether assessed empirically or, as is more often the case given a lack of data, estimated through intuition.

Systemic risks go beyond systematic factors; they involve severe shocks that have the potential to re-align entire markets in unpredictable ways. An example of such an extreme event is the remote but non-negligible potential that today’s so-called “proxy wars”7 escalate into a broader active conflict between great powers.8 The challenge of incorporating such eventualities into investment decision making is not only estimating appropriate probabilities that such events may occur, but establishing ideal strategic responses should they do so. Catastrophic shocks are exceedingly rare and have the potential to create winners and losers in asset markets that are difficult or impossible to predict.9 It may be more fruitful for investors to focus on more incremental — and more likely — eventualities that have the added benefit of being easier to model.

Media coverage naturally tends to focus on the national and trans-national arenas, but local political developments can be especially impactful for real estate investments. Such issues can fly under the radar, especially given many of the most relevant ones are only of interest to a specialist audience. For example, changes in policy around topics like the planning process, property taxes and transfer taxes (a.k.a. stamp duty) can have direct, measurable and immediate impacts on property cash flows and thus values. The distraction of the bright shiny lights of global geopolitics should not be allowed to excessively overshadow the critical local issues that impact real estate.

To a certain extent, political risks can be managed through diversification. This is especially true when they involve isolated events that impact one country or subnational division such as a specific city, province or state. But often political events are part of a broader arc with potentially far-reaching consequences. A smattering of small seeds can grow from obscurity into a thicket. Nothing illustrates this better than the rise of populism, nationalism and protectionism around the world, themes set to dominate elections this year and beyond. The very notion of “globalized nationalism” may sound like an oxymoron, but it has become a fact.10 While diversification is an essential portfolio construction concept that helps manage many types of risk, including political risk, care must be taken to recognize when what may appear to be “specific” risks are part of a broader pattern that is difficult to “diversify away.”

Geopolitical and political risks are difficult to incorporate into traditional financial analysis. We find that thinking through scenarios can be helpful in identifying investment themes that may emerge from geopolitical trends. These can point to strategies to avoid — as well as potential new ones to pursue. The “Looking Ahead” section of this note expands on some of the key themes we have been tracking.

As geopolitical events are difficult to control and plan for, one may conclude, similarly to that same protagonist in the Everything Everywhere film, that “nothing matters.” But uncertainty is no excuse for ignoring geopolitical risks. We do stop short of directly feeding geopolitical themes into our formal risk management program, where the focus is on the specific risks that can actively be managed for our clients.11 However, it remains important to observe and understand macro conditions from a holistic perspective. The work done in our regional research teams — particularly that focused on capital markets, the signals that foreshadow potential inflection points and the local political themes that impact real estate — is critical to this effort.

We have argued that political and geopolitical risks are difficult to incorporate into investment processes, but that considering “what ifs” can be useful in uncovering relevant investment themes. Below are three potential real estate implications of the current geopolitical backdrop that we are monitoring today:

Footnotes

1 LaSalle analysis of data from Time and our proprietary investable universe estimates. See LMQ page 5 for more detail.

2 Sources: “What do financial markets think of the 2016 election?” Brookings Institution paper, Wolfers and Zitzewitz, 2016. The article predicted that “a Trump victory would trigger an 8-10% sell-off”. See also “The Consequences of a Trump Shock,” a Project Syndicate article by Simon Johnson, 2016. He predicted Trump’s election would “likely cause the stock market to crash and plunge the world into recession.”

3 On the news of the 2016 election result, Standard & Poor’s 500-stock index initially fell 5% but ended the day up more than 1%, according to Refinitiv. The US avoided a recession until the emergence of the COVID-19 pandemic, according to Oxford Economics.

4 Source: “Biden vs Trump: Key policy implications of either presidency,” Economist Intelligence Unit, 2023.

5 Sources: “What to Expect From Divided Government.” PIMCO article, Cantrill, 2022. According to the article, “the equity markets historically have tended to do well in years of split government.”

6 Source: The Handbook of Risk Management: Implementing a Post-Crisis Corporate Culture. P. Carrel, 2012. “Systematic or market risk refers to the inherent danger present throughout the entire market that cannot be mitigated by diversifying your portfolio. Broad market risks include recessions, periods of economic weakness, wars, rising or stagnating interest rates, fluctuations in currencies or commodity prices, and other ‘big-picture’ issues like climate change. Systematic risk is embedded in the market’s overall performance and cannot be eliminated simply by diversifying assets.”

7 According to the Oxford Dictionary, “proxy wars are the replacement for states and non-state actors seeking to further their own strategic goals yet at the same time avoid engaging in direct, costly, warfare.” Various observers have argued that the Russia-Ukraine and Israel-Gaza conflicts are proxy wars. For example, see “IKs the ware in Ukraine a proxy conflict?” Kings College London report, Hugues (2022).

8 According to a research brief by RAND: “Great power wars — conflicts that involve two or more of the most powerful states in the international system. These have historically been among the most consequential international events.”

9 Source: “What a third world war would mean for investors,” The Economist, 2023. The article highlights the virtual impossibility of positioning an investment portfolio to outperform through prior world wars, even if the investor had correctly predicted that these conflicts would occur.

10 For further discussion of the global spread of nationalism, see “How cynical leaders are whipping up nationalism to win and abuse power”, The Economist, 2023; “Demonizing nationalist parties has not stemmed their rise in Europe,” The Economist, 2022; “The new nationalism,” The Economist, 2016.

11 We do, however, utilize tools that correlate to geopolitical risk. For example, the JLL Global Real Estate Transparency Index (GRETI) supports our monitoring of evolving investment conditions around the globe. Whilst the model does not explicitly consider political risk, the two are inexplicably linked through the inclusion of a number of governance and regulation data points.

12 Source: “A global economic policy uncertainty index from principal component analysis,” Finance Research Letters, Peng-Fei Dai, 2019.

13 Source: “What are the impacts of the Red Sea shipping crisis,” J.P. Morgan, 2024.

14 Source: “The Great Rewiring: How Global Supply Chains Are Reacting to Today’s Geopolitics,” Center for Strategic & International Studies, 2022.

15 Sources: “The business costs of supply chain disruption,” Economist Intelligence Unit, 2021 and “Why Deglobalization Makes US Inflation Worse,” Project Syndicate, Moyo, 2022.

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

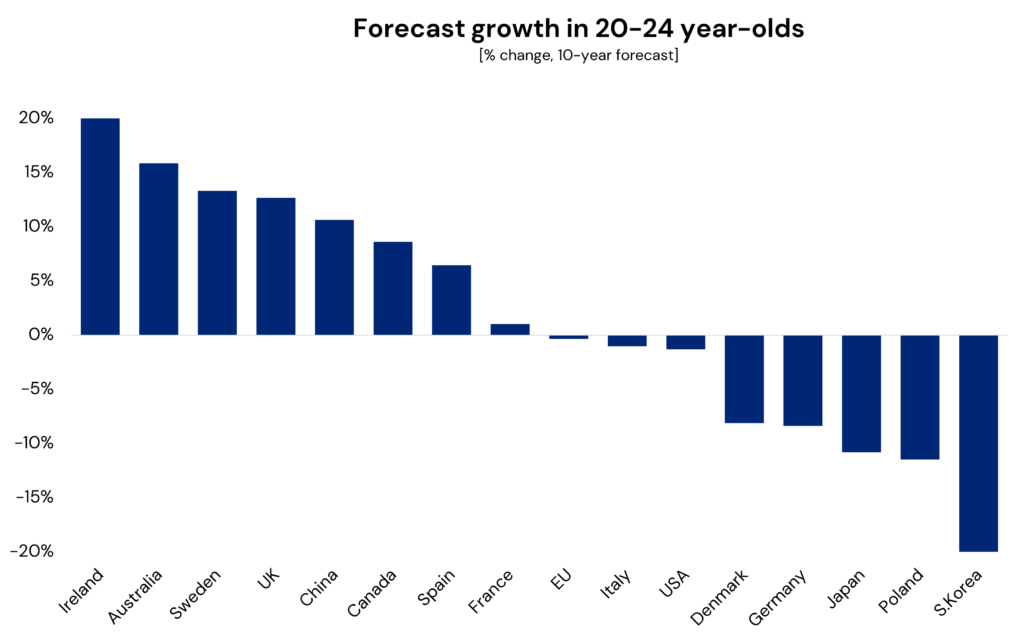

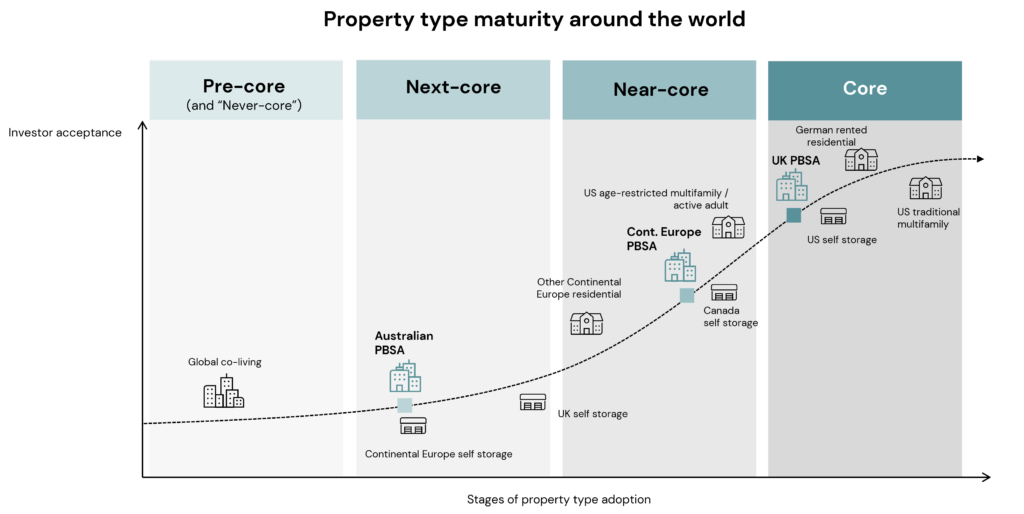

Purpose-built student accommodation (PBSA) in Europe ranks as one of our top-conviction sectors for investment in the coming years. No longer deserving of the “niche” label in the United Kingdom, it is already more institutional than any other type of living sectors property in the country and is rapidly maturing in Continental Europe as well. The rise of student accommodation on investors’ buy lists is for good reason. This ISA Briefing will set out why that is so and discuss how the sector stands out in Europe compared with student housing in the rest of the world.

After a brief, pandemic-induced interruption, in-person learning in Europe is back with more students enrolled than at any point in history. Higher education participation rates in the European Union have steadily risen across recent years, reaching an all-time high of 36% for 20-24 year-olds1 in 2021/22, with the same proportion recorded for the UK in 2023.2 A total of 18.5 million students were studying in the EU as of the 2021/22 academic year, with a further 2.9 million in the UK, having grown by 8% and 20%, respectively, over the previous five years.3

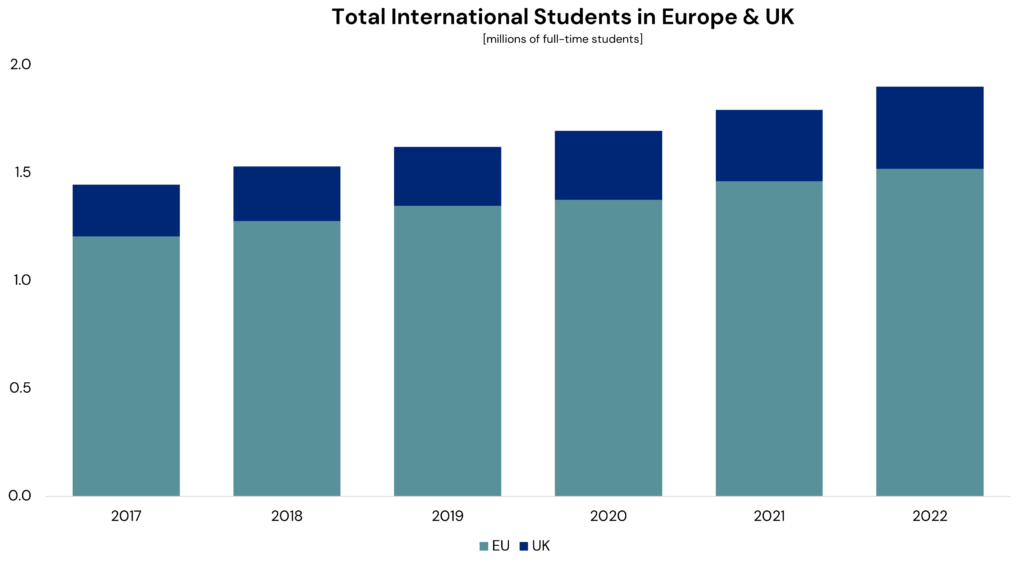

Demand for PBSA varies by profile of student. While domestic students are still crucial as a source of demand, particularly in markets where few students commute from home to study, international students are far more likely to reside in PBSA than domestic students (60% more likely to do so in the UK, as an example4). As shown in the chart below, international student mobility has been on a clear growth trend in recent years, with 2021/22 seeing a record number of foreign students in the EU and UK. European students studying outside their home countries elsewhere in Europe is a longstanding feature of the market, facilitated by freedom of movement within the EU, well-established student exchange programs, the rise of English-language courses and Europe’s dense geography.

A key driver of growth has been students from outside Europe. Europe has an outsized number of highly ranked universities relative to its size,5 a prevalence of English-language courses (which are increasingly no longer limited to the UK and Ireland) at a comparatively cheaper cost of tuition and living compared to North America.6 These attributes taken together can explain the sharp rise in non-EU students studying in the bloc, whose numbers have grown 31% since 2016.7 In the UK, the growth has been even faster, at 59% over the same period.8

That said, there are demand-side risks to be mindful of. The demographic outlook for Europe is mixed; forecasts for some countries such as the UK, Spain and Sweden show a demographic ‘bump,’ with the number of university-aged people growing ahead of national population levels. However, in other nations, numbers are forecast to be broadly flat (France) or negative (Germany and the Netherlands). This suggests uneven growth in demand for higher education going forward.9

This mixed demographic outlook will mean greater reliance on international student demand, but there are tentative signs that may also be facing some headwinds. A recent policy change in the UK has removed the right to visas for international students’ family members.10 For now, this change represents tinkering around the edges and is unlikely to have a major impact on demand. It does, however, indicate a directional change in policy aimed at restricting overseas student numbers, presumably in a bid to bring down immigration figures. Such policy changes may incrementally dissuade would-be foreign students from studying in the UK, though demand may shift elsewhere, potentially to the benefit of other European countries. Despite such risk factors, the overriding view is one of positivity for higher education demand in Europe and therefore PBSA.

European student housing should be viewed within the wider context of the region’s housing market. Europe is currently facing a long-term, persistent housing shortage. Housing scarcity is not limited to major gateway cities, but is also the reality within mid-sized cities and even smaller university towns. Since 2010, Europe has built homes at a rate only 40% below pre-GFC levels,11 contributing to rising rents, increasing house-price-to-income ratios and worsening access to suitable housing. Demand for rental housing in cities remains robust, supported by long-term trends of immigration, urbanization and declining home ownership rates; as such, the imbalance between supply and demand is now fully entrenched.12

Students are, like all participants in the housing market, at the mercy of housing supply and demand. Shortages have fed through to the student market, with students finding accommodation increasingly unaffordable. Over the past two years, this has led to sharp growth in PBSA rents, with several UK cities reporting year-over-year growth in the high teens for 2023, and other markets experiencing growth well ahead of previous levels.13 The lack of supply is also leading to students being housed increasingly in unsuitable conditions; stories from the UK of students living in hotels or in completely different cities over an hour travel from campus are a clear symptom of insufficient student housing stock.