Singapore (December 12, 2024) – Asia Pacific macroeconomies and real estate markets are showing signs of potential structural changes and unique cyclical patterns, setting the region apart from global trends.

This is the thrust of the Asia Pacific chapter of ISA Outlook 2025 report just released by LaSalle Investment Management (“LaSalle”). Published every year since 1993, LaSalle’s ISA Outlook is designed to help the real estate industry navigate the year ahead.

This year’s key findings include:

Investors in Asia Pacific real estate must navigate new investments and existing portfolios in a complex environment with signs of structural change and a distinctly different cycle compared to historical norms. These factors could have a combination of positive and negative implications for investors, some of which may only become apparent years later.

Adding to the complex macro environment is the US election result, which could lead to heightened economic uncertainty and periodic capital market volatility. China is particularly vulnerable and, to a lesser extent, Hong Kong. Beyond China and Hong Kong, it is difficult to predict clear winners or losers from the U.S. election result for now. We believe that select real estate markets or sectors could benefit from some supply chain rebalancing. In addition, investors may consider focusing on Asia Pacific real estate markets/sectors that are anchored by domestic demand and domestic capital.

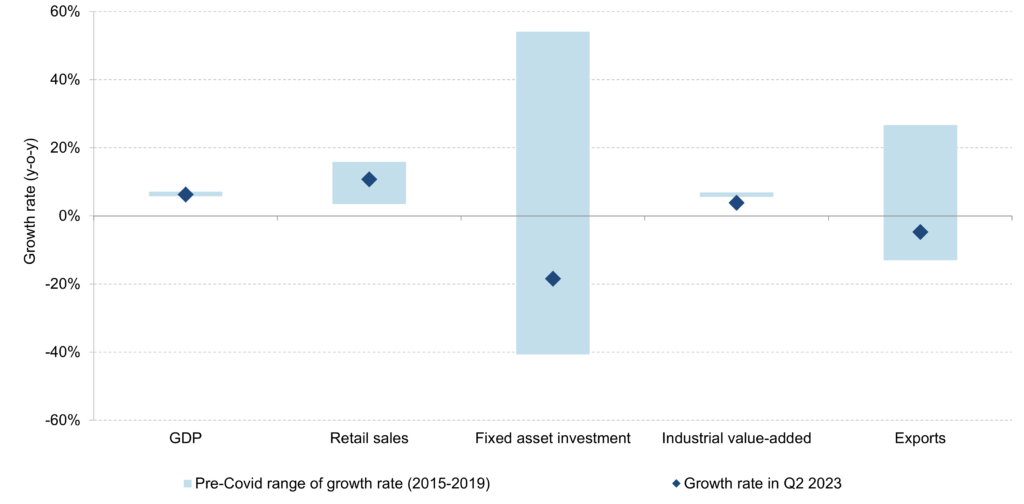

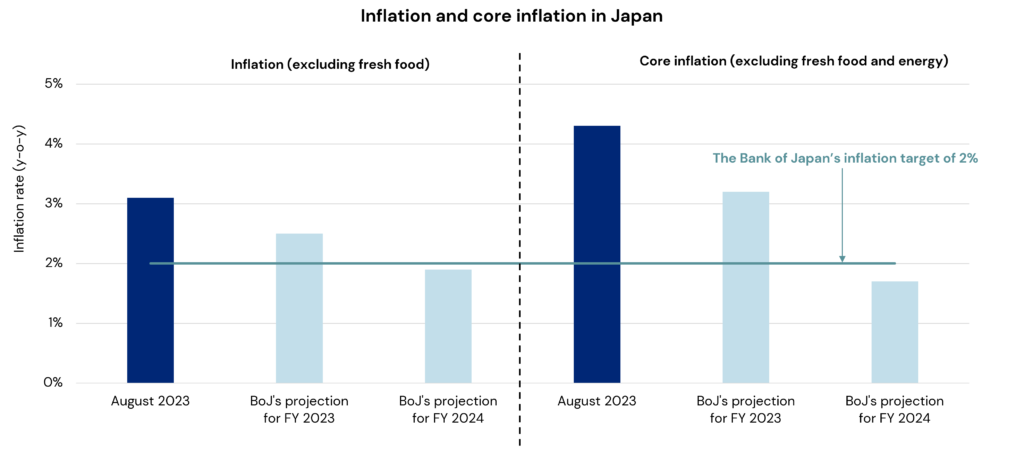

In China, which faces the weakest economic growth and consumer confidence in decades, heightened geopolitical tensions between the US and China, as well as the absence of impactful structural reforms or larger-scale stimulus packages, suggest an extended period of economic weakness. This creates a challenging environment for China’s residential and commercial real estate markets over the next few years.

Japan remains the most liquid market in the region, with inflationary growth prospects. Should the substantial domestic investor base in Japan continue to anchor the real estate capital market, the potential impact of further interest rate hikes can be limited. Nonetheless, it is essential to allow for flexibility and the potential for unexpected outcomes, when evaluating investment opportunities or setting up business plans for existing portfolios in Japan.

In other developed economies of the region, the varying and sometimes contrasting cyclical patterns among major real estate sectors within each country set the region apart from global trends.

Commercial real estate liquidity in Asia Pacific has demonstrated resilience compared to other global regions but is still constrained to varying degrees, except for Japan. The gap between buyer and seller expectations is weighing on liquidity and some investors are adopting a wait-and-see approach. Nonetheless, savvy investors understand that sometimes the best returns come from vintages in the wake of cycle turning points or when signs of structural change emerge.

Where favorable macroeconomic conditions present themselves and as global investment appetite returns, the diversity of Asia Pacific markets and sectors within the region will offer discerning investors a variety of opportunities with a wide range of risk-return profiles.

Five strategic themes are highlighted in the Asia Pacific ISA Outlook 2025:

Multi-family: At a nascent stage, except Japan

The multi-family sector in Asia Pacific is undergoing structural changes, driven primarily by demographic shifts and government policies, with significant potential for institutionalization. This sector offers a range of investment opportunities in a basket of markets except China, although it would take time to fully unlock value in this nascent sector outside of Japan due to unproven liquidity.

Office: Navigate cycle changes vs. potential for structural shifts

Office market performance across Asia Pacific varies significantly. It is increasingly important to consider the timing of entry and exit as well as risk mitigation plans. South Korean, Japanese and Singaporean offices offer strategically selected investment opportunities for investors with different risk and return appetites.

Logistics: Not a clear outperforming sector

The logistics sector shows dispersion in performance across markets, submarkets and sub-sectors. With relatively balanced supply-demand dynamics, Australia, Singapore and select Japanese markets offer investment opportunities, despite reducing return expectations.

Retail: Distinctive consumption patterns

We expect that well-managed retail assets that have adapted their tenant mixes and market positioning in response to changing consumption habits will outperform, adding to operational intensity. A granular, asset-level approach to investment is crucial, given the performance variations across markets and sub-sectors.

Hotel: Momentum mostly priced in, except Japan

The Japanese hotel market is set to continue its growth trajectory, driven primarily by domestic demand and, to a lesser extent, inbound tourists. However, the performance is expected to vary across markets and segments, influenced by the operational capability to navigate challenges such as labor shortages and rising labor costs.

Looking ahead, investors in Asia Pacific real estate must navigate a complex environment marked by structural changes and atypical market cycles.

Elysia Tse, Asia Pacific Head of Research and Strategy at LaSalle, commented: “There are many unknowns in the current complex economic climate, compounded by impending changes in Trump 2.0, which will likely lead to periodic episodes of capital market volatility. Investment strategies that favor domestic tenant demand and domestic capital, as well as those that focus on operational intensity, such as deal execution and in-house leasing, are important for value creation and preservation. In the event of significant dislocation or capital market volatility, investors could seek attractive entry points or creative, structured solutions to address capital stack issues for some troubled property owners or developers.”

Brian Klinksiek, Global Head of Research and Strategy at LaSalle, added: “As we enter 2025, we’re seeing the dawn of a new real estate cycle. While challenges remain, particularly in resolving legacy capital stack issues, we’re observing improving capital market conditions and emerging opportunities across a wide range of sectors and geographies. Investors who recognize these shifts early and act with flexibility are likely to benefit from attractive risk-adjusted returns. However, it’s crucial to remain vigilant about risks on the horizon and avoid the expectation of a rapid return to ultra-low interest rates.”

Ends

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages US$88.2 billion of assets in private and public real estate equity and debt investments as of Q3 2024. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Dec 12, 2024 LaSalle named a ‘Best Place to Work in Money Management’ by Pensions & Investments for ninth-consecutive year

LaSalle Investment Management has been named a Best Place to Work in Money Management for 2023 by Pensions & Investments (P&I).

Dec 04, 2024 LaSalle’s ISA Outlook 2025: The start of a new cycle for US and Canadian real estate

It comes as interest rates are down and economic growth concerns have begun to fade, but new risks are on the horizon.

Dec 03, 2024 LaSalle achieves four stars across all four of its 2024 PRI assessment categories

The results show improvement over last year’s assessment, in which LaSalle secured four stars in three categories.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

This article first appeared in the December 2024/January 2025 edition of PERE.

LaSalle’s Ryu Konishi and Julie Manning spoke to PERE about the growing importance of sustainability as part of investment decision-making and LaSalle’s approach to creating a global real estate net zero carbon pathway strategy.

A 360-degree approach to decarbonization

The importance of sustainability as part of investment decision-making in the real estate space has been on the rise for quite some time. In fact, the various physical risks associated with climate change, and the regulatory imperative of transitioning to net zero, are now so significant that these factors are gradually filtering through in the form of real-world valuation impacts.

For real estate investors, this raises both risks and opportunities. LaSalle Investment Management is one firm that was early to recognize this, having set up a global sustainability committee back in 2008. More recently, it has worked with the Urban Land Institute to develop a decision-making framework for assessing physical climate risk in relation to its real estate investments.

According to Julie Manning, global head of climate and carbon, and Ryu Konishi, fund manager of Lp3F (LaSalle’s global real estate net-zero strategy), this kind of approach to risk analysis – both broad and deep – is essential. So, where should investors start? And what might a determined decarbonization program in real estate look like?

Almost three years after interest rates began to spike leading into the Great Tightening Cycle, the first light of a new real estate cycle is clearly visible on the horizon. As with the start of every new day, however, opportunities and challenges lie ahead. LaSalle’s Research and Strategy team will examine both throughout the course of November and December, as we publish four separate chapters, one covering our global outlook, and three deep-dives covering the outlook for Europe, North America and Asia Pacific. Each chapter can be found alongside an accompanying video conversations with lead authors on the links below.

Chapters

In the Global chapter of ISA Outlook 2025, we look at how to make the most of this new dawn and the opportunities it may present, but with a watchful eye on ways the new day could go off track. We examine these through four broad themes in this year’s report: the morning sky, the capital stack hangover, the breakfast menu, and the early bird.

We examine each of these concepts in turn, and ask what each means for real estate and they intersect with one another and other key trends.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

While dawn is universal, across Europe it can appear different from each location and every angle. European real estate is transiting inflection points following a deep capital market correction. The INREV ODCE index shifted in the latest quarter from declines to positive after seven down quarters.

Against this backdrop, we share our Impressions of a Rising Cycle in Europe, with a focus on what makes the region different from others across the globe. We also share our five key strategy themes for investors in European real estate for the year ahead.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

The summer and autumn of 2024 saw growing optimism among real estate investors. The belief that the dawn of 2025 would open with sunny skies for the real estate market was driven by falls in interest rates from peak levels, fading economic growth concerns and real estate valuations now more aligned with market transactions.

But with more uncertainty creeping into the picture in late 2024, especially around longer-term interest rates, what we see could be described as a “partly cloudy sunrise.”

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

The current real estate cycle in Asia Pacific is not a simple repetition of a typical cycle. While Asia Pacific economies have not been immune to supply chain disruptions and elevated inflation, interest rates and construction costs, real estate capital market liquidity in the region (with the exception of China and Hong Kong) has fared much better than in other parts of the world.

In our view, the varying and sometimes contrasting cyclical patterns among major real estate sectors within each country set the region apart from global trends.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

Published every year since 1993, LaSalle’s annual ISA Outlook is designed to help our clients and partners navigate the year ahead. It brings together smart perspectives and investment ideas from our teams around the world, based on what we see across our more than 1,200 assets that span geographies, property types and risk profiles.

As always, we welcome your feedback. If you have any questions, comments or would like to learn more, please get in touch by using our Contact Us page.

LaSalle’s Matt Sgrizzi and Isabelle Brennan discuss the outlook for REITs and ask if listed real estate is about to enter a new “golden era”?

On November 19, 2024, LaSalle hosted a client webinar to discuss the outlook for listed real estate. LaSalle Global Solutions Chief Investment Officer Matt Sgrizzi offered a recap of our recent ISA Briefing: A new “golden era” for REITs and real estate? and took questions from clients in attendance.

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

This article first appeared in the November 2024 edition of IREI Americas (subscription required).

Senior real estate credit specialists from LaSalle discuss the rising significance of senior real estate mortgage credit in investment portfolios with Institutional Real Estate Investor. They explore its ability to provide steady income and downside protection, the growing role of alternative lenders, and the current market opportunity. The article examines how this strategy offers attractive risk-adjusted returns, portfolio diversification, and enhanced resilience in today’s dynamic economic environment.

We regularly receive questions about past property market dislocations and what they might tell us about today, such as: Is office the new retail?, Will the 7+ years it took retail to rebalance be a template for office? and Should we be worried about the wave of supply in US apartments?

In our latest ISA Focus report, Rebalancing past and present, we engage in patten recognition across a range of historical episodes of occupier market challenges. We present a framework for how these imbalances tend to be resolved, and discuss the range of structural and cyclical factors that drive rebalancing. We also present a selection of historical case studies from around the world, highlighting the complex nature of the rebalancing process and how it can occur not only at different speeds, but also with “bumps in the road” for investors.

We conclude the report with a refresh of our ISA Focus: Revisiting the future of office, noting in particular that there will be specific investment opportunities that arise as the current rebalancing cycle plays out.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

As traditional lenders step back, the real estate debt market is opening up new avenues for institutional investors. In a recent Q&A with IREI, LaSalle’s Jen Wichmann, Senior Strategist and SVP of Research and Strategy, discusses the evolving landscape of real estate debt investments. From long-term trends and current market opportunities to the benefits of stable cash flow and downside protection, Wichmann provides insights into the sector.

Wichmann addresses several key topics relevant to investors considering real estate debt strategies:

The $1.5 trillion commercial real estate refinancing need in 2024-2025

How real estate debt offers downside protection and stable cash flows

Opportunities in the growing European alternative credit market

Expectations for real estate debt markets in late 2024 and early 2025

One of the most important factors we consider when deciding where to invest capital is the transparency of a real estate market. This encompasses the transparency of market fundamentals and investment performance, as well as:

its legal and regulatory transparency,

the prevalence of listed vehicles,

the transparency of transactions processes, and

the transparency of reporting on sustainability factors.

During times of heightened uncertainty, transparency is more important than ever as a foundation that allows real estate occupiers, investors and lenders to operate and make decisions with confidence.

Our latest ISA Focus report, Transparency and Strategy, explores these factors and their implications for real estate investors. We release this report alongside the Global Real Estate Transparency Index (GRETI) for 2024. GRETI is a joint publication between LaSalle and our parent company, JLL, which is based on a global survey of our extensive network of real estate market experts.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

This article first appeared in the Fall 2024 edition of NAREIM Dialogues.

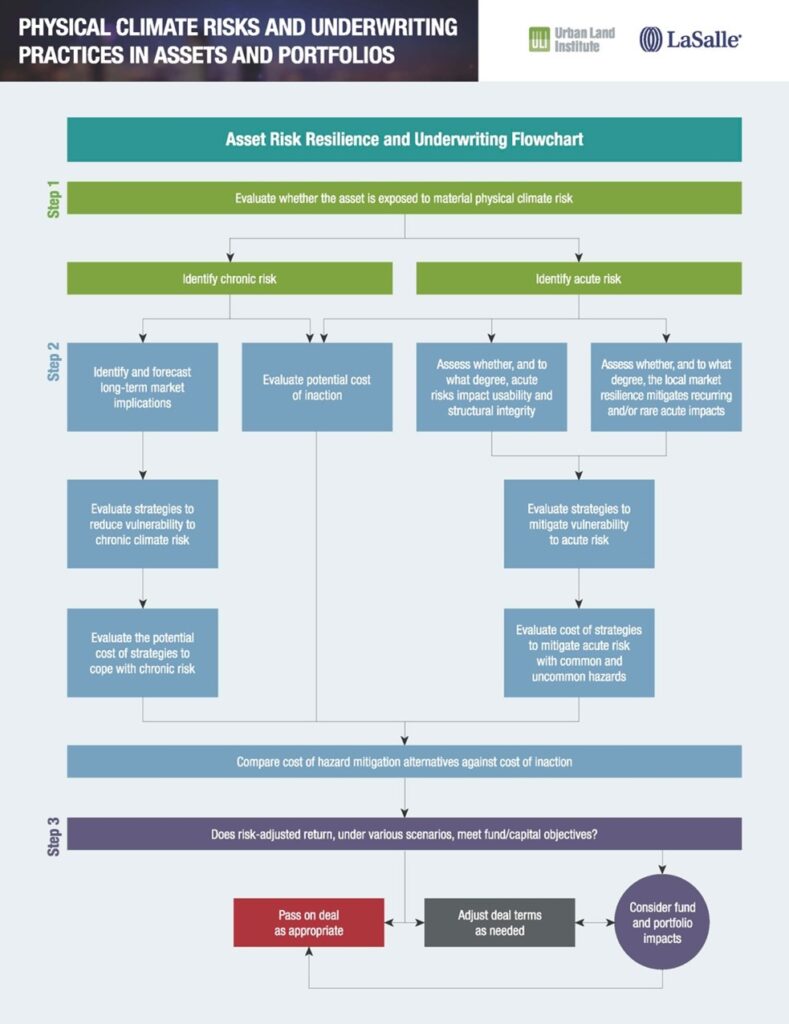

LaSalle’s Julie Manning writes about our latest report with ULI that provides an industry-wide framework for commercial real estate to address how physical climate risk data can be used in decision-making and supporting investment performance.

Using data to evaluate physical climate risk

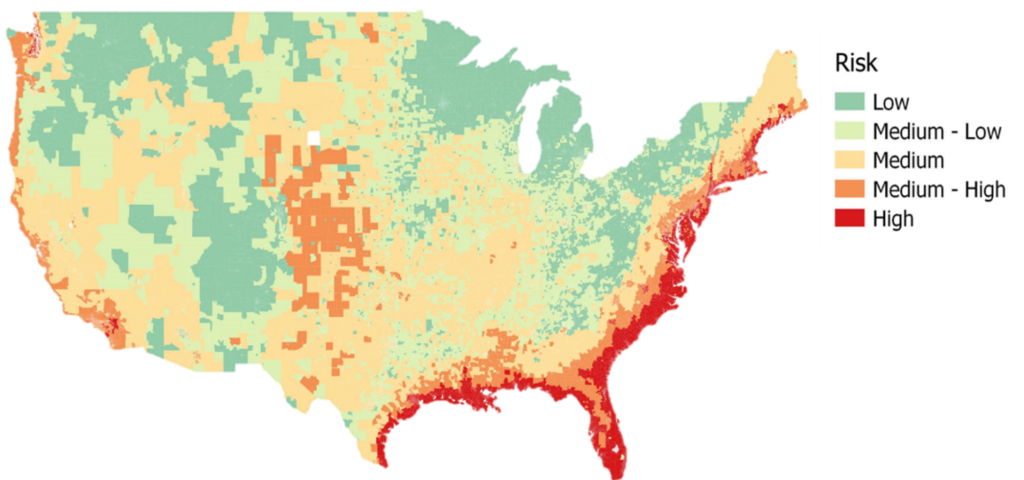

Measuring physical climate risk is of growing importance to institutional real estate managers and their investors, at both the individual property and portfolio levels. Of the $850 billion of commercial real estate assets tracked by NPI, LaSalle estimates $285 billion, or 34%, is situated in high and medium-high climate risk zones in the US.

Increasingly, being able to assess an asset’s risk exposure, and knowing how to price that risk into management strategies, are essential parts of operating a portfolio. While data is key to this assessment, understanding how to leverage the right data is even more important. With so much climate risk data available in the market, how can organizations manage and find data that gives them manageable, impactful and usable insights? And more importantly, what should managers do with these insights?

LaSalle’s Eduardo Gorab, Chris Battista and Matt Sgrizzi discuss the outlook for REITs and ask if listed real estate is about to enter a new “golden era”?

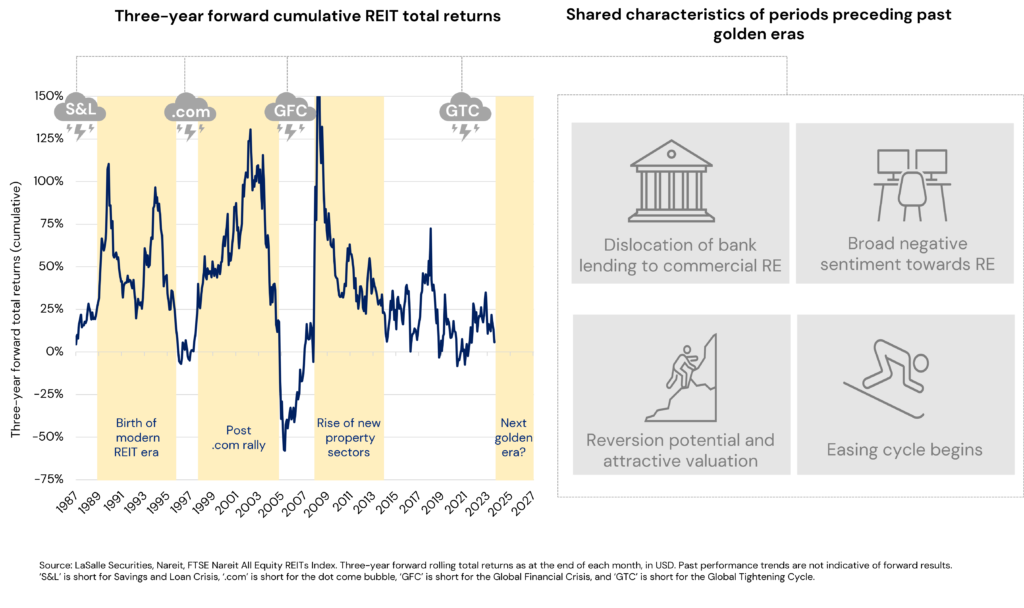

Listed real estate investment trusts (REITs) have faced a tough two and a half years, driven by the rapid tightening of financial conditions (see LaSalle Macro Quarterly, or LMQ, pg. 13). Sentiment towards REITs has been weighed down not only by the higher interest rate environment, but also by constrained bank lending, a barrage of negative headlines about commercial real estate and REIT underperformance relative to the broader equity market. But, as the saying goes, it’s often darkest before the dawn.

The modern REIT period has seen three “golden eras” of REIT investing (see chart below).1 These have been characterized by either a dramatic growth in the REIT market or outsized investment returns versus other asset classes, or both. The Savings and Loan (S&L) crisis spurred what is often considered the birth of the modern REIT era in the mid-1990s. During this period, the number of REITs increased by nearly 50%, while the market cap of that group grew nearly seven-fold. Following the Dot-com bubble, a period where REITs had been significantly out of favor, the REIT market endured a multi-year run of strong absolute performance in which it cumulatively outperformed broader equity markets by more than 300%. The period following the Global Financial Crisis (GFC) saw the rise of dynamic new property sectors in the public market, and another period of outperformance in which REITs led broader equities by 50%.

While each golden era was unique, our analysis finds that each period was preceded by challenging circumstances with four common elements (see LMQ pg. 14). These are:

dislocation of bank lending to real estate;

broad-based negative sentiment around real estate;

underperformance versus broader equities which leads to attractive relative valuation and the potential for renewed outperformance; and

an easing or reset of financial conditions, potentially aided by a central bank easing cycle.

Recent history, marked by a post-pandemic recovery followed swiftly by the Great Tightening Cycle (GTC), presents important similarities to these historical periods of severe market challenges. For instance, real estate bank lending is dislocated. An AI-driven tech frenzy and fears of a generalized “commercial” real estate malaise mean REITs have underperformed compared to equities (see LMQ pg. 22). Meanwhile, signs of an easing or stabilization in financial conditions and a potential global monetary easing cycle are becoming more apparent (see LMQ pgs. 9, 10 and 30).

While history does not repeat itself, it does often rhyme. The presence of those elements in today’s market environment, and the potential for those concerns to flip to opportunities, may foretell the next REIT golden era. We discuss each of these factors in turn.

Challenged real estate lending represents an opportunity for REITs. The past two to three years have been characterized by a significant retrenchment in bank lending to real estate. According to the US Senior Loan Officer Survey (see LMQ pg. 16), the net balance between demand for loans and banks’ willingness to lend points to the widest undersupply of credit in the past ten years, except for during the depths of COVID-19. The shortage is evident in all styles of borrowing, from riskier construction loans to mortgages backed by traditional, defensive apartment assets.

This circumstance presents an opportunity for REITs given their strong financial positions and access to the capital markets. Having learned a painful lesson from the GFC, global REITs went into the GTC with their lowest leverage levels on record (see LMQ pg. 16), and nearly 90% of their debt on fixed rates and an average remaining term of seven years.2 Looking specifically at the US market, the overwhelming majority of REIT borrowing – nearly 80% – is from the unsecured market, at rates that are today almost 100 bps lower than a traditional mortgage. This relative advantage in both access and cost of capital positions REITs to potentially play the role of aggregator and to take market share.

“Commercial” real estate negativity is office-focused, but all real estate is not office. Headlines proclaiming the demise of commercial real estate usually involve a misleading generalization. Professionally managed, income-producing real estate generally should not be conflated with office specifically. It is well known that hybrid work and other factors have harmed office values. Office fundamentals are expected to remain relatively weak,3 with the sector’s growth outlook trailing nearly all other REITs globally. Office landlords will likely need to invest capital aggressively to maintain competitiveness.

These challenging office sector dynamics have unfairly cast a shadow over the broader real estate and REIT universe. In reality, office has over time become a smaller portion of the real estate landscape, especially in the public market; as of the date of this paper, only about 6% of global REITs by market capitalization are office focused (see LMQ pg. 20).4 The public market now offers a diverse sector menu comprising a wide range of dynamic sectors. These include industrial and logistics; forms of rental residential including multi- and single-family rental, manufactured housing and student housing; various formats of healthcare property; and exposure to tech-related real estate in the form of data centers and cell towers. Sectors other than office comprise the overwhelming majority of the public REIT market,5 and many of those sectors have growth outlooks that are forecast to produce earnings growth that is in line with or better than broader equities.6 That growth outlook is underpinned by a combination of secular demand drivers and declining supply levels, the other side of the higher interest rate coin.7

Media coverage naturally tends to focus on the national and trans-national arenas, but local political developments can be especially impactful for real estate investments. Such issues can fly under the radar, especially given many of the most relevant ones are only of interest to a specialist audience. For example, changes in policy around topics like the planning process, property taxes and transfer taxes (a.k.a. stamp duty) can have direct, measurable and immediate impacts on property cash flows and thus values. The distraction of the bright shiny lights of global geopolitics should not be allowed to excessively overshadow the critical local issues that impact real estate.

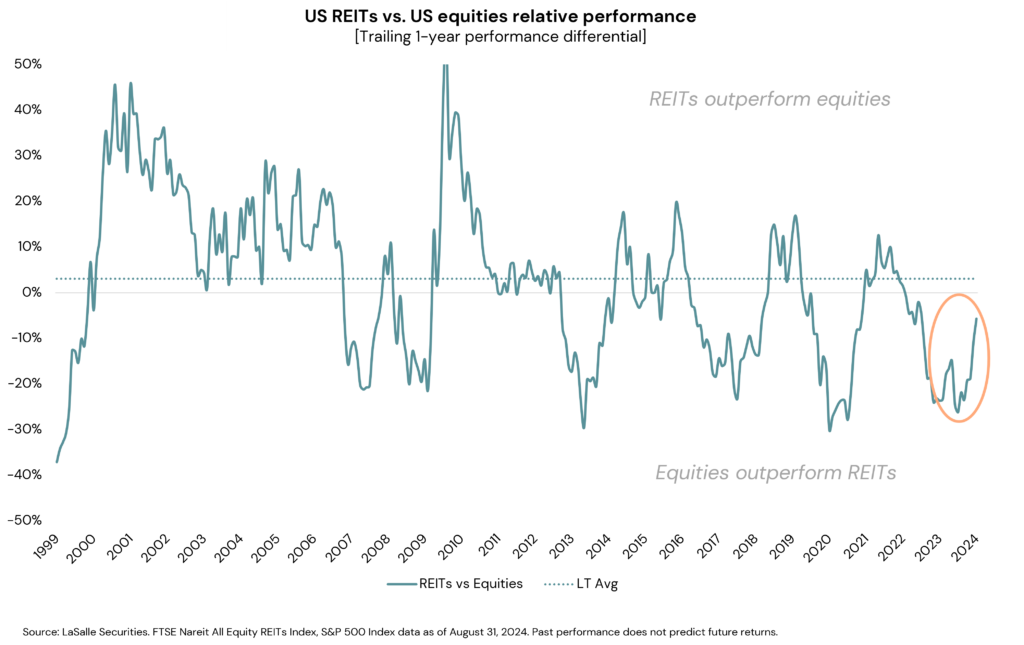

Underperformance may set the stage for a return to outperformance. The negativity around lending or financing concerns and the “death of office” have weighed on both the absolute and relative performance of REITs. The chart below shows the rolling one-year relative performance differential between REITs and equities; it indicates that REIT underperformance has reached its typical peak historical level before starting to reverse. Periods of underperformance have historically tended to reverse, and this instance is likely no different; indeed, the performance gap is already narrowing.

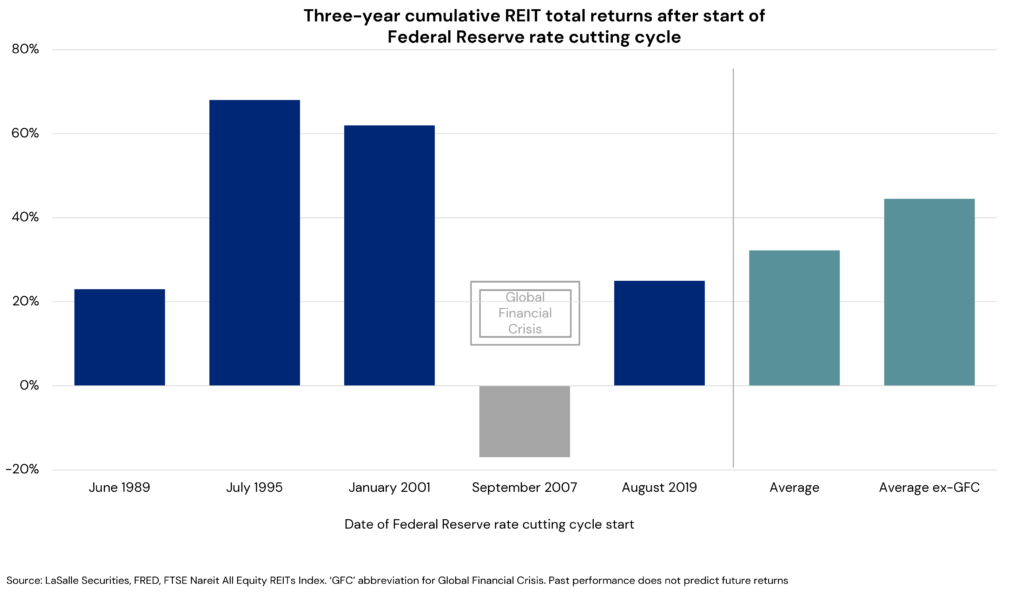

The start of a global monetary easing cycle. Real estate is a capital-intensive business that exhibits significant sensitivity to changes in financial conditions, an observation that holds for both directions of interest rate change. The downside of this dynamic was evident for much of 2022 and 2023, but the upside is likely coming into play. A global monetary easing cycle is now decidedly underway, heralded by the Fed’s 50 bps rate cut on September 18 (see LMQ pg. 31). REITs have generally performed well in periods leading up to and following a central bank easing cycle, as the chart below shows.

Over the past 25 years, REITs have produced total returns of 8% per annum, with 4-5 percentage points of that return coming from income. LaSalle’s base case underwriting for the next three years is for the REIT market to produce total returns of 9%, slightly above historical averages, with roughly four percentage points of that coming from income. That base case forecast incorporates today’s fundamental outlook and interest rate levels. Should any further easing in financial conditions occur, even only in the amount of 50 bps or 100 bps, those return expectations increase to 13% and 18% per annum, respectively, in line with previous “golden eras.”

LOOKING AHEAD >

Pattern recognition is a useful approach that can help in predicting regime shifts in market conditions. Our study of historical periods of listed REIT under- and outperformance identifies a clear pattern. Namely, there are four common factors that have driven REIT strength after a period of challenges: dislocated bank finance, weak sentiment, underperformance versus broader equities, and the start of an easing in financial conditions.

We also identify three historical “golden eras” for REITs — all of which were preceded by periods characterized by those four factors. These periods are those immediately in the wake of the S&L crisis, the Dot-com bust and the GFC.

The current environment resembles the set up for these historical golden eras, suggesting that the REIT market may be on the cusp of its next golden era of investment, according to our analysis.

Many of the factors supporting the REIT market’s upbeat prospects are also positives for real estate as a whole. For example, an easing in financial conditions has historically been a driver of strong forward REIT returns, as well as those for private equity real estate.

That said, some of the dynamics are more specific to listed real estate markets. For example, REITs’ strong balance sheets and the cost of capital advantage of their unsecured borrowing options versus conventional mortgages positions listed players to seize opportunities.

Footnotes

1 This analysis based on LaSalle Securities analysis of historical macroeconomic, capital market and listed market trends. Source for the REIT performance data cited below are the FTSE Nareit indices. 2 Source for debt pricing comments in this paragraph: S&P Global Market Intelligence, Green Street Advisors, company financial releases, company research and market analysis conducted by LaSalle Securities. 3 There is considerable global variation in office performance, and there are certainly exceptions to this generalization, especially in select Asia-Pacific markets and the higher end of the European office quality spectrum. For more discussion of global office trends, see our ISA Outlook 2024 Mid-Year Update. 4 Source: LaSalle Securities. Percent of companies classified as office focused within the global listed universe defined as the constituents of the S&P Developed REIT, FTSE EPRA Nareit Developed and Nareit All Equity Indices. Sector classifications determined by LaSalle Securities. 5 As measured by market capitalization. Source: LaSalle Securities. Global listed universe defined by the constituents of the S&P Developed REIT, FTSE EPRA Nareit Developed and Nareit All Equity Indices. Sector classifications determined by LaSalle Securities. 6 As based on LaSalle Securities proprietary modelling and consensus earnings forecasts for the Bloomberg World Index, a proxy for broader equity markets. 7 Higher interest rates mean development proformas use higher exit yield assumptions and more expensive development finance. When interest rates are high, all else being equal, the rents required to justify development are higher. 8 Based on proprietary internal LaSalle Investment Management modeling of securities returns. There is no guarantee that such forecasted returns, or any other returns referred afterwards, will materialize.

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

A prudent person sees trouble coming and ducks. A simpleton walks in blindly and is clobbered. — Proverbs 22:3

King Solomon’s words of wisdom have been passed down to us for 3,000 years. They still resonate, especially in this modern translation,1 even though the “trouble” is no longer invading Assyrians or Babylonians but the type of danger we bring on ourselves through an all-too-human combination of ingenuity, hubris and ignorance.

Watch any movie from the 1930s to the 1960s and you will see actors inhaling tobacco smoke with abandon. We know better now. Like the generational awareness of the harm caused by tobacco products, real estate owners have gradually become aware of the dangers lurking in certain building materials and contaminated soil. Starting in the 1960s, societies have spent fortunes cleaning up “miracle products.” Asbestos, PCBs, dry cleaning solvents, herbicides and lead pipes were all considered state-of-the-art technologies at various points in human history. None of these inventions were designed with the intention of killing people. They all started with a noble purpose – whether suppressing catastrophic fires, insulating transformers, cleaning wool suits or producing a pleasing nicotine buzz that also curbed the appetite. The “externalities” associated with societal damage from the use of these products took decades to discover and billions to eradicate.

Greenhouse gas emissions share a common ancestry with these miracle products. Heating buildings with diesel fuels, running gas lines through city streets, producing electricity with coal-fired plants—these were all logical, economical, and sensible solutions to the problem of bringing energy to homes, businesses and buildings of all types. The industrial revolution accelerated the growth of cities and raised the quality of life for millions of people by dragging them out of rural poverty. As we now know, society’s dependence on fossil fuels creates new problems which must be dealt with.

The recognition that miracle products can carry hidden (or not so hidden) dangers follows a predictable pattern. Here is what the step-by-step process often looks like:

Evidence and awareness. An environmental problem often requires decades of scientific study and mountains of evidence to convince people that a change is necessary. Even as this evidence accumulates, vested interests organize counterattacks to convince society that the problem is non-existent or over-stated. Eventually the harm to human life becomes so obvious that denial becomes a “fringe position.”

Market demand. In many cases, the process of partial “market adjustment” can begin ahead of government action. Voluntary data collection and industry-led reforms start the slow process of change. In the case of greenhouse gases, the marginal contribution of each emitter is so small, and so embedded in society, that government interventions sometimes lag market-led shifts (e.g., the adoption of LED lighting or heat pumps).

Regulatory response. Yet, government interventions are almost always needed to accelerate and complete behavioral change to truly eliminate harm to the environment and to human life created by “externalities.” These regulations and policy responses often get pushback as competing outcomes are debated in the political arena. Economists agree that putting a price on carbon would be the most efficient and effective solution, but a market mechanism for carbon pricing requires government intervention — in the form of a carbon “tax” or to set up an emissions trading scheme.

Benchmarks and best practices. Eventually, the rise of data benchmarks and peer group comparisons begins to shed light on who, where and how successful “treatments” are applied to any environmental problem. Engineering and laboratory science helps inform this stage of the process, as does public health or industry group data. Integration with market investment processes and decisions leads to a focus on reversing years of damage to the environment and compliance with new regulations and guidelines. At this stage, market-driven and regulatory-driven changes start to converge.

Price integration. Feedback loops are established where type 1 errors (false positives) and type 2 errors (false negative—or overlooked problems) are exposed.2 In loosely regulated situations like climate change, the efficient market hypothesis (EMH) takes hold as the change process gets partially or fully priced by consumers and producers. Economists and policy analysts favor the practice of placing a “price” on an externality to compensate society for the harm. In practice, though, compensatory payments to offset environmental damage are often decided through the courts and litigation.

Continued market and regulatory evolution. The enforcement of tighter regulations also follows its own trajectory depending on the governance structure of a particular country or urban jurisdiction and the toxicity of the problem. The discipline of epidemiology, using population data and public health analysis, is especially helpful at this stage of refining the policy solutions.

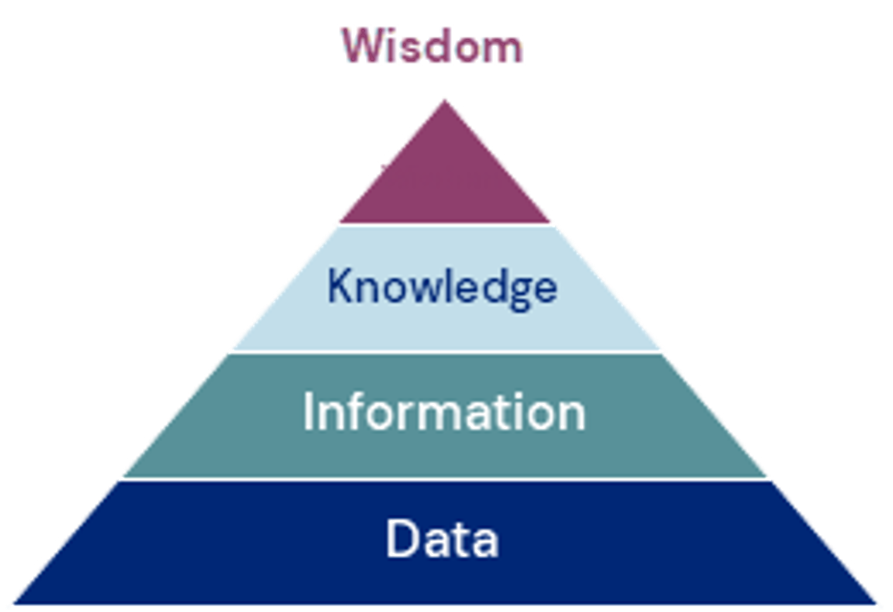

The Transition from “Data” to “Wisdom”

For the de-carbonization of buildings, various markets and countries are well into Step 3 (Regulatory Response) and Step 4 (Benchmarks and Best Practices). In Europe the “theory of change” is focused more on EU-wide or national policies to promote energy disclosures through top-down regulatory solutions. In the United States, the emphasis is based more on voluntary pledges, market solutions and regulations that are based on specific local jurisdictions. In most developed countries, steps 5 (Price Integration) and 6 (Market and Regulatory Evolution) are underway, but both have a long way to go.

The rise of real estate sustainability benchmarks (like GRESB) has accelerated in recent years. In many cases, they have expanded to include social factors and tenant well-being alongside environmental metrics. The next hurdle, though, is to establish materiality tests that infuse meaning, and determine financial impacts based on the volumes of reporting that the industry has started to produce and disclose.

Reading through ESG reports often reveals the triumph of reporting and public relations over salience or relevance. The conjoint challenges of reducing building emissions alongside improving the well-being of building users and the surrounding communities can be obscured by data denominated in less familiar metrics like tons of CO2 or Kilowatt hours. In time, and with experience, the emphasis will shift to what truly moves the needle on all elements of the “sustainable investing” paradigm—and which metrics give off misleading or meaningless “virtue” signals.

Financial metrics align most closely with the “fiduciary duty” of an investor. Moreover, stakeholders have decades of experience analyzing and interpreting financial data. It will take additional time and effort to convert environmental data into financial terms or to simply raise the consciousness of how to interpret energy and emission data in its own right. (LaSalle’s work on the “Value of Green” synthesizes studies of the evidence linking sustainability metrics and financial outcomes. An update on this work is below.)

In writing Proverbs, King Solomon gathered centuries of wisdom based on experience. In the modern world, we often believe that the steps to wisdom are built on a foundation of knowledge, information, and data. The famous “DIKW” hierarchy has been a mainstay of information sciences since the 1930s. Sustainability wisdom is still in the process of being formulated and likely requires more time to make progress. Fortunately, the foundations of this wisdom are already being put in place—first through data (the modern way to refer to many, many experiences), then information (organized and analyzed data), eventually leading to knowledge (patterns are identified and the “what” and “why” questions are answered) and finally reaching the status of accumulated wisdom (how to respond). This is a path that humans have traveled before. More lives are at stake this time around and the wisdom may not be easily agreed upon by all industries, countries and stakeholders. Nevertheless, the search for sustainability wisdom must continue and time is of the essence.

Revisiting LaSalle’s “Value of Green”

In September 2023, LaSalle published our ISA Focus report What is the value of green? Looking at the evidence linking sustainability and real estate outcomes. The report presents a framework on how sustainable attributes of properties can be viewed as both as drivers and protectors of value, along with showcasing findings from the broader literature. We continue to maintain a Value of Green tracker, monitoring research on this subject as it is produced. Some of the findings that have surfaced since the release of our initial report are worth highlighting:

In early 2024, CBRE reported in their UK sustainability index that efficient properties outperformed inefficient properties by close to 2% per year in terms of total return, over the course of 2023 across three major property types. The efficiency of buildings was delineated through EPC ratings.

UBS reported in late 2023 that a green premium of 28% and 19% in price per square foot was in evidence in the New York and London office markets, respectively, when comparing office transactions based on LEED/BREEAM certifications. This premium was also established in cap rates, showing a 36 and 27 bps premium for New York and London respectively.

MSCI published a report on price premiums for green buildings, and how they have changed over time. Looking at offices in Paris and London, a clear trend emerged from 2019 onwards showing a growing sale-price gap between offices with and without sustainability ratings. In the case of London, the gap was close to non-existent before 2019 and had since grown to 25% as of the latest reported data point in late 2022.

Beyond the direct links between sustainability and historical investment performance in terms of return, rent and value premiums, more signals are emerging as available data on the topic grows, and becomes increasingly forward looking:

In 2024, JLL published in their “Green Tipping Point“ report on how the supply/demand balance is shifting in favour of sustainable offices across the globe, as tenant demand evolves. JLL projects a 70% unmet demand across 21 global office markets.

Beyond results based on backward-looking data, detailed case studies of investments into sustainable initiatives are being published. The JLL report “Future-Proof Your Investments“ showcased opportunities for sustainable New York offices; another example is CBRE’s report “The impact of on-site rooftop solar on logistics property values.”

Sources: CBRE (March 2024) UK Sustainability Index Results to Q4 2023. CBRE P. Torres, G. Bolino, P. Stepan (2024) The Green Tipping Point. JLL T.Leahy (2022) London and Paris Offices: Green Premium Emerges. MSCI P. Torres, J. del Alamo (July 2024) Future-proof your investments. JLL D. Marina, J. Tromp, T. Vezyridis, O. Bruusgaard (July 2023) The impact of on-site rooftop solar PV on logistics property values. CBRE O. Muir, Y. Chen, T. Metcalf et.al (Dec 2023) Green premium: Study of New York and London Real Estate finds strong evidence for a ‘green premium’. UBS

What can we learn from simulations?

The de-carbonization of buildings is taking place in a complex and ever-changing environment. It is a multi-dimensional problem replete with uncertain outcomes, regulatory change, shifting societal norms and markets, and the politicization of sensitive issues.

At the June 2024 MIT World Real Estate Forum, Professor Roberto Rigobon unveiled a “sustainability simulation” game patterned on his pathbreaking work on social preferences for the European Commission. The technique shows how the traditional economic conceit that we make “resource trade-offs” does not accurately capture how humans make decisions when faced with multi-dimensional choices.

In the simulation, the audience was given nine choices for different retrofit projects for a commercial building. Each choice resulted in simultaneous movement across three metrics that the audience had already established that they cared about — changes in NOI (profitability), CO2 emissions, and tenant satisfaction/well-being. The cost of the projects was amortized into the NOI calculations and the other metrics were also calibrated based on actual data from the US.

The simulation showed that a knowledgeable real estate audience rarely solves just for “pure profits” at the expense of tenant well-being or CO2 emissions. The simulation also mimicked reality—where sometimes profitability moves in synch with reduced CO2 emissions and other times it moves it moves in the opposite direction. The simulation was designed to show how the co-movement depends on the local market and the type of de-carbonization project. Tenant well-being and CO2 emissions could be implicitly linked to revenue when and if participants believe that occupancy, rents and capital raising are all interconnected.

Through their choices, the audience tried to optimize across all three priorities at once — leading to an interesting result that revealed their average willingness to “pay” to reduce a ton of CO2 emissions of about $200 ton. Yet, if asked directly how much they would pay to reduce a ton of greenhouse gas coming from a building, it seems unlikely that many would have volunteered to pay that much. This finding also shows how the language of profitability and returns is much more advanced than the metrics and concepts associated with either decarbonization or tenant satisfaction. And that all these metrics are linked, but not fully integrated in the minds of real estate professionals.

Only a few participants in the game focused only on reducing CO2 (at the expense of decent profits). And just a few focused exclusively on profitability at the expense of tenant satisfaction or CO2 emissions. This seems like a reasonable facsimile of what enlightened investors will do — especially when they know that their actions are being disclosed. As we learn more from these simulations, it is possible that policy makers will be able to refine the mix of incentives and regulations that govern the real estate industry.

Jacques Gordon Cambridge, Massachusetts

LOOKING AHEAD >

As we advance through the six stages of market wisdom, sustainable features in real estate move away from purely “virtuous” and toward increasingly meaningful drivers of investment value. As noted in our ”Value of Green” report the challenge for investors is understanding where, when and how sustainability is driving performance, which is highly variable across markets and sectors. Given LaSalle’s global reach, we are well positioned to observe, learn and act to enhance and protect asset values for our clients, and gain and share wisdom in the process.

Markets are shifting towards wider alignment with a more sustainable future, new data and findings are continuously published. At LaSalle we also focus on the data generated within our walls, linking our own initiatives driving sustainability with their associated investment outcomes, bringing our own data and experience into the DIKW hierarchy.

Recognizing the importance of meaningful benchmarks to drive decision-making (Stage 4), LaSalle has been leading an industry initiative to develop an improved solution for decarbonization pathways in the US and Canada, which could be adopted by CRREM and others globally. More meaningful decarbonization pathways will help investors properly measure transition risks and set targets, setting the industry up to make real progress in decarbonizing the built environment.

Evolution over the Six Stages will likely be uneven over time, geography and investor type. This unevenness could provide investors at more advanced stages an advantage over less progressed investors. For instance, an investor who has incorporated a carbon business case into their investment process is at an advantage to appropriately price opportunities. For example, it should help investors identify attractive brown-to-green strategies.

Footnotes

1The Message, translated from the Hebrew scriptures by Eugene Peterson (1993-2002).

2 These are all part of the learning that occurs with any “treatment hypothesis.” The science of public health provides solid evidence to weigh whether the “treatment” is helping, hurting or having no impact on the eradication of the underlying disease. In real estate, a good example of this is the gradual discovery that with certain types of asbestos, it is more dangerous to remove it than to “encapsulate” it in an existing structure. The science of “decarbonization” is still being established to determine whether, for example, the mass production of lithium batteries does as much harm as the burning of fossil fuels. For real estate and climate change, the “treatment” will likely focus on energy efficiency/ decarbonization interventions that are a combination of government penalties/incentives and voluntary actions. The effectiveness of these treatments will depend on compliance, market response, and how well interventions find acceptance through the political process.

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Seoul (August 19, 2024) — LaSalle Investment Management Co., Ltd. (“LaSalle Korea”), on behalf of its Korea logistics investment joint venture with a Middle Eastern sovereign wealth fund (“the Joint Venture”) as well as LaSalle Asia Opportunity Fund VI (“the Fund”), has acquired two dry-only logistics facilities in Anseong within Greater Seoul with a combined gross floor area (GFA) of 385,946 square meters, at a purchase price of approximately US$450 million (or KRW5.3 million per pyung).

The two facilities are located next to each other and are built with modern warehouse specifications including spacious yards for its tenants and direct ramp access to each floor with leasable area efficiency of approximately 99%. The latter is a distinct feature for the facilities, compared to other similar sized warehouses designed with circular ramps which significantly reduces net leasable area.

Center-A, with GFA of 187,226 square meters was completed in June 2023 with 100% occupancy and Weighted Average Lease Expiry (WALE) of 4.35 years.

Center-B, with GFA of 198,718 square meters was recently completed in July 2024 and also has 100% occupancy with WALE of 4.55 years.

Across Center-A and Center-B, which will be renamed Logiport Anseong Center-I and Logiport Anseong Center-II respectively, there are four institutional tenants representing established companies in their respective industries, including semiconductor, pharmaceutical, beauty and consumer goods.

This transaction follows the acquisition of two logistics facilities in Icheon made by LaSalle Korea last year, also on behalf of the Joint Venture and the Fund. LaSalle Korea also divested a separate cold storage warehouse project this year for KRW10.4 million per pyung after completing ground-up development and stabilizing leasing on the asset.

Anseong logistics facilities

Steve Hyung Kim, Senior Managing Director and Head of Korea, commented: “The logistics sector continues to be one of the most dislocated property types requiring a high level of deal selectivity. LaSalle Korea’s recent acquisitions represent unique opportunities to invest in newly-built modern warehouses with full occupancy by institutional tenants, purchased at well below replacement costs. LaSalle Korea also plans to upgrade and implement new sustainability initiatives across these two investments which total over 4.15 million square feet in GFA.”

End

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over US $87 billion of assets in private and public real estate equity and debt investments as of Q1 2024. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Dec 12, 2024 LaSalle’s ISA Outlook 2025: Potential structural changes and distinctive cyclical patterns offer APAC opportunities

It comes as interest rates are down and economic growth concerns have begun to fade, but new risks are on the horizon.

Dec 12, 2024 LaSalle named a ‘Best Place to Work in Money Management’ by Pensions & Investments for ninth-consecutive year

LaSalle Investment Management has been named a Best Place to Work in Money Management for 2023 by Pensions & Investments (P&I).

Dec 04, 2024 LaSalle’s ISA Outlook 2025: The start of a new cycle for US and Canadian real estate

It comes as interest rates are down and economic growth concerns have begun to fade, but new risks are on the horizon.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

Seoul (July 30, 2024) — LaSalle Investment Management Co., Ltd. (“LaSalle Korea”), on behalf of LaSalle Asia Opportunity Fund VI (“the Fund”) and a local co-investor, was awarded an office site in Seoul after submitting the winning bid in the 5th round of a non-performing loan (NPL) collateral auction. The winning bid price of approximately US$115 million represented a 33% discount to its appraised value. The land site is walking distance from Gangnam Station within the Gangnam Business District, with existing zoning to allow development of a new office with planned GFA of over 29,000 square meters. The project cost upon completion is estimated to be approximately US$245 million.

Artist’s impression of the new office development in Gangnam Business District

This acquisition marks the Fund’s second foray into the office market in Korea following a high-yield loan deal last year to bridge finance a 10-storey office project in Seoul’s Seongsu district. This collateralized loan was priced during a period of credit spread dislocation and was successfully repaid on its maturity date in December 2023, allowing the Fund to exit its first opportunistic debt investment in Asia Pacific.

Amongst key gateway city office markets globally, Seoul’s Gangnam office district continues to display post-pandemic resilience supported by both occupier demand and capital markets liquidity. According to JLL REIS and JLL Korea Research, as of Q1 2024, the office vacancy rate in Gangnam was 0.3%, the lowest compared to the two other business districts in Seoul with net effective rents also registering the highest year on year increase compared to the other business districts.

Steve Hyung Kim, Senior Managing Director and Head of Korea, commented: “Opportunistic investing in a higher cost of capital environment has forced us to be patient and also creative in how we source attractive entry points to our acquisitions. On behalf of our investors, we recently closed on recapitalizations, private off-market sales, and collateral acquisitions from NPL auctions like this recent transaction which capitalizes on both Gangnam’s strong office fundamentals, as well as a lowered project cost basis due to a legacy borrower and junior lender getting foreclosed. Larger sized office sites in Gangnam have retained scarcity value and this latest project from LaSalle Korea will introduce modern designs and sustainability initiatives to which we are very excited about.”

End

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over US $87 billion of assets in private and public real estate equity and debt investments as of Q1 2024. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Dec 12, 2024 LaSalle’s ISA Outlook 2025: Potential structural changes and distinctive cyclical patterns offer APAC opportunities

It comes as interest rates are down and economic growth concerns have begun to fade, but new risks are on the horizon.

Dec 12, 2024 LaSalle named a ‘Best Place to Work in Money Management’ by Pensions & Investments for ninth-consecutive year

LaSalle Investment Management has been named a Best Place to Work in Money Management for 2023 by Pensions & Investments (P&I).

Dec 04, 2024 LaSalle’s ISA Outlook 2025: The start of a new cycle for US and Canadian real estate

It comes as interest rates are down and economic growth concerns have begun to fade, but new risks are on the horizon.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

Joelle Chen joined LaSalle in 2024 and is responsible for defining LaSalle’s Asia Pacific sustainability strategy, leveraging technical capabilities and organizational best practices to drive sustainability performance.

She was formerly the Head of Sustainability Asia for Lendlease, delivering net zero investment roadmaps for its portfolio, and instrumental in reducing the embodied carbon of new developments through active supplier engagement to reduce cost impacts to projects. She was the first Asia Pacific Head for World Green Building Council and previously headed the Smart Sustainable Cities team at the Singapore Economic Development Board, driving public-private partnerships through innovation platforms.

Joelle graduated from the National University of Singapore with a Master of Architecture and a Master of Business Administration from the Singapore Management University.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

TE Capital Partners (“TE Capital”) and LaSalle Investment Management (“LaSalle”) jointly announced the sales launch of Visioncrest Orchard, a freehold Grade A commercial strata development located in the heart of Singapore’s prime Orchard Road precinct, with a combined office and retail area of 154,711 sqft (14,373 sqm). TE Capital is the operator for Visioncrest Orchard and the partners are accompanied in the joint venture by Metro Holdings as a capital partner of the TE Capital-managed vehicle.

Visioncrest Orchard, Singapore

As part of the launch, a 14,725 sqft office space on Level 6 and a 14,844 sqft office space on Level 9 have been released for sale at S$3,980 psf and S$4,130 psf respectively. Following VIP previews in June, a 14,725 sqft office space and several retail units spanning 1,388 sqft are currently under due diligence.

TE Capital and LaSalle attribute the strong demand for the LEED Gold certified, 11-storey freehold office to the allure of the Orchard submarket as well as the asset’s outstanding core qualities which have been boosted by substantial enhancements.

Located along Penang Road, Visioncrest Orchard offers easy walking access to Dhoby Ghaut and Somerset Mass Rapid Transit (MRT) stations, with direct access to three train lines (North-South, North-East and Circle lines). The Central Expressway (CTE) and Pan Island Expressway (PIE) expressways can be reached within a few minutes’ drive.

Situated just over 400 meters (437 yards) from Plaza Singapura and 550 meters (601 yards) from 313@Somerset, Visioncrest Orchard occupies a strategic position close to Orchard’s vibrant retail scene while being just a stone’s throw away from Singapore’s central business district. It is also nestled within the exclusive Oxley enclave and Istana, the official residence and office of the president of Singapore, providing a coveted address which combines prestige with cultural and historical significance.

Offices at Visioncrest Orchard boast greenery views through expansive full-glass, solar-protected windows with floor to floor heights reaching 4.3 meters. Large floorplates of approximately 14,500 sqft offer numerous possibilities for customization, while a generous provision of 135 onsite parking lots offer convenience for occupiers. Smart fittings that offer user-friendly building access via self-registration e-kiosks, as well as enhanced security through biometric features such as facial recognition are among the upgrades that occupiers can expect, while amenities such as a swimming pool, a well-equipped gym, a tennis court and other recreational facilities promote the integration of wellness with work.

In the years to come, Visioncrest Orchard is expected to benefit from commitments by the Singapore government to revitalize the Orchard district. Initiatives such as the Strategic Development Incentive (SDI) scheme will see the introduction of broadened urban planning parameters such as increased building heights, expanded gross floor area and more flexible land use permissions on older assets. Plans to pedestrianize parts of Orchard and redesign traffic flows will also contribute to the transformation of the area. As the availability of high-quality, high-specification freehold offices in the Orchard district will continue to be limited, the partners expect interest in Visioncrest Orchard to remain robust.

CBRE, ERA, JLL, Knight Frank, PropNex and Savills have been appointed as agents for Visioncrest Orchard.

About TE Capital Partners

TE Capital Partners is a uniquely positioned real estate investment and fund management firm, equipped with development management capabilities that focuses on APAC real estate markets. Established in 2019, TE Capital Partners is backed by the family office of Mr Teo Tong Lim, Group Managing Director of Tong Eng Group, a real estate company with a history of more than 80 years, having owned and developed close to 200 acres of land, comprising mixed-use, office, retail, landed housing and apartments.

As of Q4 2023, TE Capital Partners and its subsidiaries, has an AUM of more than S$3 billion across Singapore, Australia, Japan and the United States, and the Principals have developed more than S$3 billion of commercial office, residential and mixed development projects in Singapore in recent years, such as Solitaire on Cecil. Some commercial projects under management include 350 Queen Steet and 312 St Kilda Road in Melbourne, Australia. For more information, please visit www.tecapitalasia.com and LinkedIn.

NOTE: This press release may contain forward-looking statements by TE Capital Partners and should not be relied upon by readers and/or investors for any purposes. This is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. No representation or warranty express or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this press release. Actual performance, outcomes and results may differ from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions.

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately US$87 billion of assets in private equity, debt and public real estate investments as of Q1 2024. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.