Brian Klinksiek

Global Head of Research and Strategy

Almost three years after interest rates began to spike leading into the Great Tightening Cycle, the first light of a new real estate cycle is clearly visible on the horizon. As with the start of every new day, however, opportunities and challenges lie ahead. LaSalle’s Research and Strategy team will examine both throughout the course of November and December, as we publish four separate chapters, one covering our global outlook, and three deep-dives covering the outlook for Europe, North America and Asia Pacific. Each chapter can be found alongside an accompanying video conversations with lead authors on the links below.

In the Global chapter of ISA Outlook 2025, we look at how to make the most of this new dawn and the opportunities it may present, but with a watchful eye on ways the new day could go off track. We examine these through four broad themes in this year’s report: the morning sky, the capital stack hangover, the breakfast menu, and the early bird.

We examine each of these concepts in turn, and ask what each means for real estate and they intersect with one another and other key trends.

Global Head of Research and Strategy

Managing Director, Global Research and Strategy

While dawn is universal, across Europe it can appear different from each location and every angle. European real estate is transiting inflection points following a deep capital market correction. The INREV ODCE index shifted in the latest quarter from declines to positive after seven down quarters.

Against this backdrop, we share our Impressions of a Rising Cycle in Europe, with a focus on what makes the region different from others across the globe. We also share our five key strategy themes for investors in European real estate for the year ahead.

Europe Head of Research and Strategy

Europe Head of Core and Core-plus Research and Strategy

Europe Head of Debt and Value-add Capital Research and Strategy

The summer and autumn of 2024 saw growing optimism among real estate investors. The belief that the dawn of 2025 would open with sunny skies for the real estate market was driven by falls in interest rates from peak levels, fading economic growth concerns and real estate valuations now more aligned with market transactions.

But with more uncertainty creeping into the picture in late 2024, especially around longer-term interest rates, what we see could be described as a “partly cloudy sunrise.”

Americas Head of Research and Strategy

Canada Head of Research and Strategy

The current real estate cycle in Asia Pacific is not a simple repetition of a typical cycle. While Asia Pacific economies have not been immune to supply chain disruptions and elevated inflation, interest rates and construction costs, real estate capital market liquidity in the region (with the exception of China and Hong Kong) has fared much better than in other parts of the world.

In our view, the varying and sometimes contrasting cyclical patterns among major real estate sectors within each country set the region apart from global trends.

Asia Pacific Head of Research and Strategy

Vice President, Strategist

China Head of Research and Strategy

Published every year since 1993, LaSalle’s annual ISA Outlook is designed to help our clients and partners navigate the year ahead. It brings together smart perspectives and investment ideas from our teams around the world, based on what we see across our more than 1,200 assets that span geographies, property types and risk profiles.

As always, we welcome your feedback. If you have any questions, comments or would like to learn more,

please get in touch by using our Contact Us page.

Last year, we released the inaugural edition of LaSalle’s ISA Portfolio View, where we discussed the art and science of portfolio construction and why it matters most when market conditions change suddenly. That was certainly true at the time of last year’s release and remains so today.

In this year’s edition, we cover the five foundational concepts of portfolio management below, and how they should be considered alongside an investor’s objectives and values to devise a strategy for their portfolio.

Why real estate lays out the case for property exposure in a multi-asset context?

Why real estate lays out the case for property exposure in a multi-asset context?  Why global considers the benefits of expanding horizons beyond an investor’s domestic market?

Why global considers the benefits of expanding horizons beyond an investor’s domestic market?  Why be sector smart tries to make sense of the recent changes in relative sector performance with an eye to building resilient portfolios?

Why be sector smart tries to make sense of the recent changes in relative sector performance with an eye to building resilient portfolios?  Why be quadrant smart addresses the interplay among the “four quadrants” of real estate?

Why be quadrant smart addresses the interplay among the “four quadrants” of real estate?  Why manage risk explores the importance of—and our approach to—managing investment risk?

Why manage risk explores the importance of—and our approach to—managing investment risk? For 2024, we have also updated ISA Portfolio View to include the most recent available data, and added new sections on:

The speed and unpredictability of market changes over the last few years highlights the importance of not only planning ahead by thinking carefully about how to create real estate portfolios that can be expected to be resilient, but also working with an asset-class expert who understands the nuances presented by real estate.

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

CHICAGO (September 17, 2024) – Elena Alschuler, LaSalle’s Americas Head of Sustainability has been recognized with the Nareit 2024 Sustainable Leadership Award on behalf of JLL Income Property Trust.

Nareit presented the inaugural Sustainability Impact Awards at its REITworks: 2024 Sustainability & Social Responsibility Conference in McLean, VA. The awards recognize REITs for implementing sustainable practices that demonstrate leadership, ingenuity, and environmental impact in the commercial real estate industry.

Elena was recognized for her leadership in sustainability in the built environment, and her collaboration with industry peers to share knowledge and develop best practices. This is exemplified in Elena’s recent role as chair for the CRREM North America Working Group which is working to develop decarbonization pathways to benchmark transition risk.

Nareit Senior Vice President of Environmental Stewardship & Sustainability, Jessica Long said: “We are excited to highlight Elena and JLL Income Property Trust who are raising the bar for advancing sustainability practices in their operations, buildings, communities, and across the broader REIT and commercial real estate industry.”

LaSalle Global Head of Climate and Carbon, Julie Manning said: “This award is a well-deserved recognition of Elena’s exceptional contributions to sustainable real estate practices. Her innovative strategies and tireless efforts have not only elevated LaSalle’s program but are also working to set new benchmarks for the entire industry. Elena’s work exemplifies our commitment to exploring sustainable solutions that can drive investment performance.”

JLL Income Property Trust, President and CEO, Allan Swaringen said: “At JLL Income Property Trust, we believe sustainability initiatives can drive value and mitigate risk. We integrate these sustainability principles in our portfolio construction, acquisitions and asset management activities, resulting in a tailored approach to each property in our portfolio. Elena has been at the forefront of driving these efforts, and this recognition by Nareit is a testament to her commitment.”

ENDS

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages US$84.8 billion of assets in private and public real estate equity and debt investments as of Q2 2024. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments.

For more information, please visit www.lasalle.com, and LinkedIn.

About JLL Income Property Trust, Inc. (NASDAQ: ZIPTAX; ZIPTMX; ZIPIAX; ZIPIMX)

JLL Income Property Trust, Inc. (NASDAQ: ZIPTAX; ZIPTMX; ZIPIAX; ZIPIMX), is a daily NAV REIT that owns and manages a diversified portfolio of high quality, income-producing apartment, industrial, grocery-anchored retail, healthcare and office properties located in the United States. JLL Income Property Trust expects to further diversify its real estate portfolio over time, including on a global basis.

About Nareit

Nareit serves as the worldwide representative voice for REITs and publicly traded real estate companies with an interest in U.S. real estate. Nareit’s members are REITs and other real estate companies throughout the world that own, operate, and finance income-producing real estate, as well as those firms and individuals who advise, study, and service those businesses. Nareit’s focus is to broaden and deepen REIT ownership to help a growing set of everyday American investors enjoy the benefits of holding real estate in a well-diversified portfolio, while increasing capital sources that invest in America’s future. Nareit is the exclusive registered trademark of the National Association of Real Estate Investment Trusts, Inc.®, 1875 I St., NW, Suite 500, Washington, DC 20006-5413. Follow us on REIT.com. Copyright© 2024 by Nareit®. All rights reserved.

London (March 11, 2024) – LaSalle Investment Management (“LaSalle”), the global real estate investment manager, has appointed Bouygues Rénovation Privée (“Bouygues”) as the main contractor for the redevelopment of Bergère, a landmark office-led, highly-amenitized workspace project in Paris.

Situated in the 9th Arrondissement, Bergère is in a prime location in the heart of Paris, surrounded by a thriving cluster of companies from across technology, fashion, and financial and professional services. It forms part of a vibrant urban environment with a high concentration of restaurants, bars, shops, department stores, and cultural and leisure facilities. Positioned just 150 metres from the Grands Boulevards metro station, Bergère also benefits from convenient transport links and access to three of Paris’s largest transportation hubs: Gare du Nord, Saint Lazare and Chatelet – Les Halles. The renovated building will have a floor area of approximately 26,850 square meters and was redesigned by the leading French architectural firm PCA-Stream.

Scheduled for completion in Q1 2026, the redevelopment of Bergère will incorporate industry-leading sustainability practices. This will involve a sensitive restoration of the building’s architectural heritage while upgrading the technical equipment to meet operational Net Zero Carbon goals. The project will prioritise the reuse of materials to minimise the projected embodied carbon associated, and the building is targeting a BREEAM Excellent certification, with a 50% reduction in operational CO2e and a 20% reduction in embodied CO2e compared with the benchmark for Parisian office renovations.

The redevelopment will also look to meet future tenant requirements and evolving work trends with high-quality amenities to promote in-person interaction and facilitate a hybrid working, including an auditorium, business centre, bars and restaurants, event spaces and a media broadcast studio.

Marc Fauchille, Head of Development and Repurposing, Europe, LaSalle Investment Management, commented: “We are excited to work together with the experience and expertise at Bouygues Bâtiment Ile-de-France on Bergère, to create an innovative and truly revolutionary workspace in the heart of Paris. Bergère is set to be a prime office-led development in Paris, situated in a highly sought-after location in one of the strongest European markets. The project is already attracting a high level of tenant interest given its quality, location and sustainability credentials.”

Thomas Rousseau, Managing Director of Bouygues Bâtiment Ile-de-France Rénovation Privée, adds: “We are very proud to have been selected by LaSalle Investment Management for this Parisian prime office restructuring operation, which is also listed as a Historic Monument. The teams were particularly driven by the ambition of the project, the technical complexity as well as the challenges in terms of uses and the environment. This success is the result of collective work. Our teams are already mobilized to highlight their expertise and know-how in heritage restoration, our core business. This building is a real showcase for our company in terms of decarbonization, exemplarity and innovation. A big thank you to LaSalle Investment Management and its partners for trusting us with the realization of this exceptional project.

LaSalle acquired Bergère, on behalf of Encore+, its flagship open-ended pan-European fund, in May 2020 from BNP Paribas in a sale-and-leaseback transaction.

Ends

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages approximately US $90 billion of assets in private and public real estate equity and debt investments as of Q4 2024. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information, please visit www.lasalle.com, and LinkedIn.

Marketing Disclaimer: This information is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for information purposes only and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results. Please refer to the offering documents Encore+ for detailed information on the risks, reward and performance information of the Fund.

CHICAGO (January 11, 2024) – LaSalle Investment Management (LaSalle) has closed on the acquisition of Canal Crossing Logistics Center, a core industrial warehouse located in Phoenix, AZ. The acquisition was made on behalf of the firm’s U.S. core open-ended fund LaSalle Property Fund (LPF).

The property is 100% leased to a leading provider of alternative aftermarket, specialty salvage and recycled auto parts to repair and accessorize vehicles. The tenant is a wholly owned subsidiary of LKQ Corporation (Nasdaq: LKQ), which has operations in North America, Europe and Taiwan. The property is centrally located in the Sky Harbor Airport submarket, offering immediate access to major transportation corridors and connectivity to the Phoenix metropolitan area. Built in 2015, the property features a highly functional site plan with Class A building specifications.

Jim Garvey, President and Portfolio Manager, LaSalle Property Fund said: “This acquisition is a great fit for our portfolio and reflects our strategy to increase the Fund’s industrial allocation through investment in infill submarkets within high-growth metropolitan markets.”

Matt Bogovich, Vice President of Transactions added: “We are pleased to have acquired such a high-quality industrial asset in a strategic infill submarket of Phoenix. The Airport Submarket is the most established industrial cluster in the MSA, and this asset stands out given its newer construction and modern features.”

About LaSalle Property Fund

LaSalle Property Fund invests in and manages a portfolio of diversified high-quality core real estate assets in major markets across the US in the industrial, multifamily, office, retail and niche sectors. Since its inception in 2010, LaSalle Property Fund has focused on creating and managing a portfolio with an emphasis on property types with strong growth potential and lesser risk of disruption from secular changes. The Fund’s assets are diversified across major and niche property sectors in major American markets, aiming to provide reliable returns.

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over $89 billion of assets in private and public real estate equity and debt investments as of Q3 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit http://www.lasalle.com, and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

MONTREAL (December 20, 2023) – Ivanhoé Cambridge (“IC”) announced today that it has syndicated a 49% stake of Vaughan Mills shopping center to LaSalle Investment Management (“LaSalle”), as part of a syndication process. The 49% share represents one of the largest retail transactions Ivanhoé Cambridge has made over the past few years.

Per the syndication terms, Ivanhoé Cambridge and LaSalle will serve as co-owners, as IC will continue to act as asset manager in executing the property business plan.

“We are thrilled to share the news of this enhanced partnership with LaSalle, a sophisticated player who will contribute to the continued success of this property,” said Annie Houle, Head of Canada at Ivanhoé Cambridge. “Vaughan Mills is a prominent shopping center that has stood out over the past twenty years, highlighting the strength of retail.”

“We are pleased to continue to build a successful relationship with Ivanhoé Cambridge, a valued best-in-class global partner and real estate leader,” said Stephen Robertson, Head of Canada Transactions at LaSalle.

Stuart Sziklas, Senior Managing Director and Portfolio Manager at LaSalle, added, “Winning retail centers have remained quite resilient through cycles, and Vaughan Mills’ leasing and occupancy track record highlights its premier location and status in the market.”

Located in Vaughan, Ontario, Vaughan Mills is visited by over 13 million people annually. The shopping center stands out thanks to its unique positioning, a distinctive 1.7 km, 1 level “race track-style” configuration, and its retail offering of both regular and outlet brands, with a strong focus on entertainment and leisure.

Vaughan Mills is 97% leased, with a significant mix of international and national brands. The shopping center underwent an expansion in 2015 and is certified BOMA Best Platinum, the highest level for this program supporting smart and sustainable building operations worldwide.

CBRE Limited acted as real estate advisors and RBC Capital Markets Realty Inc. acted as financial advisors to Ivanhoé Cambridge.

About Ivanhoé Cambridge

Ivanhoé Cambridge develops and invests in high-quality real estate properties, projects and companies that are shaping the urban fabric in dynamic cities around the world. It does so responsibly, with a view to generate long-term performance. Ivanhoé Cambridge is committed to creating living spaces that foster the well-being of people and communities, while reducing its environmental footprint.

Ivanhoé Cambridge invests internationally alongside strategic partners and major real estate funds that are leaders in their markets. Through subsidiaries and partnerships, the company holds interests in 1,500 buildings, primarily in the industrial and logistics, office, residential and retail sectors. Ivanhoé Cambridge held C$77 billion in real estate assets as of December 31, 2022, and is a real estate subsidiary of CDPQ (cdpq.com), a global investment group. For more information: ivanhoecambridge.com.

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over $89 billion of assets in private and public real estate property and debt investments as of Q3 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit http://www.lasalle.com, and LinkedIn.

CHICAGO (December 11, 2023) – LaSalle Investment Management (LaSalle) is pleased to announce it has been named a Best Place to Work in Money Management for 2023 by Pensions & Investments (P&I). This marks the eighth consecutive year LaSalle has received this prestigious recognition.

Presented by Pensions & Investments, the 12th annual survey and recognition program is dedicated to identifying and recognizing the best employers in the money management industry.

Kristy Heuberger, LaSalle Americas Co-Head, said: “Being honored as a ‘Best Place to Work’ for an eighth year is a testament to the foundational elements of LaSalle’s success: our people and our culture. We’re proud that the culture every employee at LaSalle works hard to foster continues to be recognized.”

Brad Gries, LaSalle Americas Co-Head, added: “Our culture is reflected in everything we do at LaSalle, whether it’s providing exceptional client service,driving investment performance, developing talent, growing careers, or simply making LaSalle a place that people enjoy coming to work. We thank our employees for continuing to make our firm a Best Place to Work in Money Management.”

P&I Chief Operating Officer Nikki Pirrello said: “A strong workplace culture that supports talent, advocates progress and drives innovation is paramount to driving the best outcomes and these asset managers demonstrate that. Congratulations to the 2023 honorees for their commitment to employee well-being, attractive incentive structures and talent development that demonstrate how investing in your employees can elevate our industry to greater heights.”

P&I Executive Editor Julie Tatge said: “As their employees attest, the companies named to this year’s Best Places to Work list demonstrate a commitment to building and maintaining a strong workplace culture. Even as firms grappled with volatile markets and ongoing stresses from the pandemic, their employees said they felt strong support from their managers, enabling them to do their best work.’’

Pensions & Investments partnered with Best Companies Group, a research firm specializing in identifying great places to work, to conduct a two-part survey process of employers and their employees. The first part consisted of evaluating each nominated company’s workplace policies, practices, philosophy, systems and demographics. This part of the process was worth approximately 25% of the total evaluation. The second part consisted of an employee survey to measure the employee experience. This part of the process was worth approximately 75% of the total evaluation. The combined scores determined the top companies. For a complete list of the 2023 Pensions & Investments Best Places to Work in Money Management winners and write-ups, go to www.pionline.com/BPTW2023.

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over $89 billion of assets in private and public real estate property and debt investments as of Q3 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit http://www.lasalle.com, and LinkedIn.

London (December 11, 2023) – LaSalle Investment Management (“LaSalle”), the global real estate investment manager, has secured planning permission to redevelop and refurbish Bergère – a landmark office-led, highly-amenitized workspace project in Paris.

The building is renowned for its striking façade and exceptional architectural features, such as the main atrium and the monumental staircase. Redesigned by the leading French architectural firm PCA-Stream, the redevelopment is expected to complete by Q1 2026 and will have a lettable floor area of approximately 26,500 square meters.

Located in the 9th Arrondissement, in the heart of Paris, the building is in a prime location surrounded by a thriving cluster of companies from across technology, fashion, and financial and professional services. It forms part of a vibrant urban environment with a high concentration of restaurants, bars, shops, department stores, and cultural and leisure facilities. The demand-supply imbalance for office space in the area remains acute, with Paris CBD vacancy at 1.9% compared to a European average of 7.4% as of Q3 2023, according to JLL. The area also boasts excellent transport links, just 150 metres from the Grands Boulevards metro station, providing immediate access to three of Paris’s largest transportation hubs: Gare du Nord, Saint Lazare and Chatelet – Les Halles.

The new development will meet future tenant requirements and evolving work trends, offering state-of-the-art environmental performance ratings with high-quality amenities. These include amenities to promote in-person interaction and hybrid working, including an auditorium, business center, bars and restaurants, event spaces and a media broadcast studio. It will house 442 bicycle parking spaces, with direct access from the street, as well as changing rooms, fitness facilities and 75 EV charging stations. It will also comprise street-facing food and beverage, and a retail unit designated for affordable rent for social impact-related businesses to support the local community. It will also increase the site’s green outdoor space by 50% to more than 2,000 sqm, including a garden, two court yards and two rooftop terraces.

The project will be redeveloped with industry-leading sustainability processes and credentials in mind. This comprehensive development will involve a sensitive restoration of the building’s architectural heritage while upgrading the technical equipment to meet operational Net Zero Carbon goals. It will also prioritise the reuse of materials to reduce the projected embodied carbon associated with the project.

The building aims for a BREEAM Excellent and HQE Excellent certification with a 50% reduction in operational CO2e, and a BBCA (Bâtiment Bas Carbone) targeting a 20% reduction in embodied CO2e compared to existing Parisian office refurbishment benchmarks. It will also target the BiodiverCity label for its increase in green space and biodiversity onsite, and the project has been designed to meet the Décret Tertiaire 2050 requirements.

LaSalle has appointed JLL as principal leasing agent, with CBRE and BNP Paribas.

David Ironside, Fund Manager of LaSalle Encore+, commented: “The refurbishment and redevelopment of Bergère will provide a truly revolutionary workspace in the heart of Paris. The European office market has become polarised, with performance increasingly distinguished by quality, location and sustainability credentials. There is growing demand for centrally-located, recently refurbished assets with superior environmental performance ratings that align with the new standards of tenant expectations. Bergère will meet all these demands, and we are excited to unveil this new development.”

Marc Fauchille, Head of Development and Re-purposing, Europe, LaSalle Investment Management, added: “Central Paris is one of the strongest European office markets, with extremely low vacancy rates and rising demand for the highest quality space. We expect this highly amentizied building will benefit from increasing rental growth due to its outstanding central location and features that appeal to tenants and the people who work, live and socialise in this area. We will also be allocating space to support local social impact-related business, which we hope can make a real positive difference in the neighbouring community.”

LaSalle acquired Bergère, on behalf of Encore+, its flagship open-ended pan-European fund, in May 2020 from BNP Paribas in a sale-and-leaseback transaction.

Ends

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages approximately $78 billion of assets in private and public real estate property and debt investments as of Q1 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information, please visit www.lasalle.com, and LinkedIn.

Marketing Disclaimer: This information is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for information purposes only and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results. Please refer to the offering documents Encore+ for detailed information on the risks, reward and performance information of the Fund.

On November 28, LaSalle’s Global Head of Research and Strategy, Brian Klinksiek, gave a keynote address at Canadian Real Estate Forum’s annual Global Property Market conference in Toronto where he discussed our global real estate investment themes for 2024:

These themes are discussed in detail in ISA Outlook 2024, our annual publication designed to help our clients and partners navigate the year ahead. It brings together smart perspectives and investment ideas from our teams around the world, based on what we see across our more than 1,500 assets that span geographies, property types and risk profiles.

CHICAGO (Dec. 5, 2023) – The US and Canadian real estate markets continue to see subdued transaction volume and a wait-and-see approach from investors amid their respective central banks’ campaigns to snuff out inflation through interest rate hikes. LaSalle’s Insights, Strategy and Analysis (ISA) Outlook 2024 makes the case that secular trends, not cyclical trends, may hold answers as to where winning property types will land in 2024, with the early half of the year looking similar to 2023 and the potential for a rebound later in the year.

The report will be released in regional chapters throughout November and December, and can be viewed at: www.lasalle.com/Outlook2024.

The ISA Outlook 2024 looks at five key themes from a global and regional level:

On a broad basis in the Americas, the report observes a potential recovery later in 2024, a continued focus on interest rates and their impact and the potential for supply weighing on real estate fundamentals.

Brian Klinksiek, Global Head of Research and Strategy at LaSalle, said: “Significant unknowns remain in the global real estate market as we head into 2024, including interest rates, geopolitical tensions, and whether major economies may tip into recession. While it’s very difficult to time markets, data on previous down cycles suggest that it’s often during unsettled periods that savvy investors can find strong value in real estate, making this a potentially strong vintage for investment.”

Select ISA Outlook 2024 findings for North America include:

Rich Kleinman, Co-CIO and Head of Research & Strategy for the Americas at LaSalle, said, “Looking at real estate investment solely through the lens of interest rates means you’re missing the bigger picture as we believe sectors and markets will adjust to rates at varying speeds. Investors with dry powder, flexibility and who can identify price gaps are likely to come out as winners in this transitional market.”

Chris Langstaff, Head of Research & Strategy for Canada at LaSalle, said, “Looking to 2024, we expect that in the midst of a continued softening of the Canadian economy in the near term, the strong migration trends will support long-term growth of the Canadian economy. This will particularly benefit the apartment and industrial sectors when economic growth resumes.”

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages approximately $89 billion of assets in private and public real estate property and debt investments as of Q3 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. The firm sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information, please visit www.lasalle.com, and LinkedIn.

Forward looking statement

The information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

LONDON (29 November 2023) – Despite a challenging macroeconomic picture, European real estate has begun to acclimatise to higher interest rates and will offer some of the world’s most attractive supply-demand dynamics next year, according to the Insights, Strategy and Analysis (ISA) Outlook 2024 report published by global real estate investment manager LaSalle Investment Management (“LaSalle”).

Last year’s report predicted European macro headwinds and a stall in capital markets activity, but also strong real estate market fundamentals. Looking ahead, the 2024 ISA Outlook for Europe describes how investors that are ready to move out of waiting mode, with realistic expectations for operating income growth, can find compelling new investment opportunities.

This year’s report identifies five trends that differentiate Europe and earn the region’s real estate assets an important place in investors’ property portfolios:

These trends are driving demand in particular for logistics and rental housing, as well as superior performance by offices in the ‘super-prime’ segment.

Macro challenges but appealing supply-demand dynamics

Having defied expectations of a recession in 2023, Europe still faces elevated recession risk. Inflation has begun to abate but proven comparatively stubborn, particularly in the UK, inducing higher policy rates from the ECB and Bank of England. As the delayed impact of rising rates begins to bite, European property markets enter 2024 searching for a clear peak in interest rates – as well as an end to the war in Ukraine.

Europe’s occupational fundamentals are coming off the boil of recent years, with rental growth set to cool to its lowest level since 2020 next year. However, we expect that average rent growth should remain positive, especially for logistics and rental housing – even in an economic downturn – helped by low vacancy rates relative to history.

In logistics, while demand has cooled across Europe and vacancy is ticking up from extremely low levels, a shrinking construction pipeline means that the long-term revenue growth outlook remains very bright. The scope for further e-commerce market penetration is, conversely, a headwind for European retail. However, assets such as outlet centers with turnover-linked leases have lifted revenues in line with nominal sales growth.

Investors in Europe can access strategies rooted in barriers to supply, arising from Europe’s high (and rising) constraints on development. Nowhere does this apply more than in the residential sector, where the undersupply is chronic, while migration powers long-term demand growth. Surging student demand and rising mortgage rates are causing people to rent for longer and until later in life, boosting demand further in Purpose-Built Student Accommodation and rental housing specifically.

Opportunities on the leading edge of offices

European city centers are returning to their pre-Covid levels of vibrancy, attracting office occupiers and capital to more central locations. To better understand how this spectrum of office quality is evolving, we recommend going beyond ‘bifurcation’ alone in segmenting the market. The widening gaps between leading and lagging offices are determined by a range of many factors like location, design, amenities and sustainability.

In London, “super-prime” office buildings command significant rent premiums to “prime” averages. Since 2019, the UK capital’s median office relocation was from a non-BREEAM-rated EPC-D building to BREEAM Excellent / EPC-B or better. Across Paris and London, new offices’ vacancy rate is c.2%, three times less than for second-hand offices. Notably, centrally located, modern offices in Paris and Munich have defied subdued transaction levels and remain liquid, with sales attracting respectable bidder pools.

Alternative lenders gain momentum

Outside of these pockets of investment activity, alternative lenders are well positioned to solve capital stack equations in 2024, filling gaps created by banks’ reduction in LTVs to provide debt financing that generates attractive risk-adjusted returns.

Dan Mahoney, Head of European Research and Strategy at LaSalle, said: “What we are seeing in Europe is real estate markets beginning to acclimatise to the higher-rate environment and gradually shift out of the waiting mode that has chilled transaction volumes in 2023. The continent’s distinct combination of rebounding city vibrancy, high supply barriers and compelling conditions for debt make it an important allocation in global real estate portfolios.”

Brian Klinksiek, Global Head of Research and Strategy at LaSalle, added: “Significant unknowns remain in the global real estate market as we head into 2024, including interest rates, geopolitical tensions, and whether major economies may tip into recession. While it’s very difficult to time markets, data on previous down cycles suggest that it’s often during unsettled periods that savvy investors can find strong value in real estate, making this a potentially strong vintage for investment.”

Ends

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages approximately $78 billion of assets in private and public real estate property and debt investments as of Q1 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information, please visit www.lasalle.com, and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

SINGAPORE (November 16, 2023) — LaSalle announced today that a fund it manages (the “fund”), in a joint venture with TE Capital Partners (“TEC”), has executed a Put and Call Option Agreement (“PCOA”) to acquire a 11-storey Grade A office building at 103 Penang Road, Singapore 238467, also known as VisionCrest Commercial (the “asset”). The joint venture is operated by a subsidiary of TEC.

Part of VisionCrest, a mixed-use development that also comprises a gazetted national monument, the House of Tan Yeok Nee, as well as four residential blocks with 265 units in total, the asset includes retail space on the ground floor.

The freehold, high-spec, LEED Gold certified asset, which has a strata area of 154,711 square feet, is centrally located in Singapore’s prime Orchard Road precinct, with excellent connectivity including a 5-minute walk to Dhoby Ghaut Mass Rapid Transit (MRT) Station, which is served by three major train lines (North-South, North-East and Circle Lines). Not only does the asset enjoy immediate access to abundant retail, dining, entertainment and accommodation options at its doorstep, it is also expected to benefit from the Urban Redevelopment Authority’s plan to rejuvenate the Orchard Road precinct to strengthen its position as one of Asia’s most sought after retail and commercial corridors.

The asset offers a strong cash flow profile, with an occupancy rate of 99% that is backed by a diverse roster of multinational tenants including Manulife Financial Advisers, Puma Sports SEA Trading and The Coffee Bean & Tea Leaf.

As the second project by the joint venture between TEC and the fund, this transaction reflects the managers’ confidence in the stability and resilience of Singapore’s office sector, as well as its potential for mid- to long-term capital value growth and preservation.

George Goh, Head of Acquisitions and Asset Management, Southeast Asia, LaSalle Investment Management said, “We are pleased to extend the strong and fruitful partnership we’ve had with TEC. This asset is a very rare freehold offering in a well-performing market, with potential for value-add and growth.”

Claire Tang, Co-CIO Asia Pacific, LaSalle Investment Management said, “This asset is a strategic addition to the fund’s portfolio as we respond to the continued interest of global institutional investors and private investors in the Singapore’s office sector, buoyed by sustained occupier demand in this market.”

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages over $78 billion of assets in private and public real estate property and debt investments as of Q1 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

With shifting interest rates, dynamic occupier fundamentals and deepening bifurcation within sectors, ISA Outlook 2024 asks how real estate investors should respond to rapidly changing market conditions. To answer these questions and more, we published four separate chapters covering the global and regional outlooks over the course of November and December.

Download the full document now, or individual chapters covering the Global, European, North American and Asia Pacific outlooks are available in the tabs below.

The global macroeconomic context for real estate remains unsettled, and more so than earlier in 2023. Until late summer, interest rates in most major markets exhibited high volatility, but little overall trend. They moved mainly sideways, owing to cooling inflation and expectations that central banks were reaching the end of their tightening cycles. This was helpful in setting a pricing baseline for real estate investors. But the outlook for rates and thus real estate pricing has become more unsettled of late.

What does this mean for real estate and how does it intersect with other key trends?

Global Head of Research and Strategy

Managing Director, Global Research and Strategy

European property markets have been waiting for a peak in European Central Bank and Bank of England policy rates, for an end to the war in Ukraine and for bid-ask pricing spreads to resolve. Investors ready to move out of waiting mode in 2024 can benefit from rebased prices, opportunities to solve capital stack equations, and strong fundamentals in many sectors.

In this chapter of ISA Outlook 2024, we examine the state of the European market and conclude with recommendations for specific investment strategies – underpinned by realism and targeted toward areas of forecast resilient income growth.

Europe Head of Research and Strategy

Europe Head of Core and Core-plus Research and Strategy

Europe Head of Debt and Value-add Capital Research and Strategy

Against a volatile macroeconomic backdrop and with growth expected to slow, we believe that in 2024 it will be the trajectory of interest rates that will have the greatest impact on real estate values in the US and Canada.

As investors continue to adapt to cooler conditions, this chapter of ISA Outlook 2024 examines the current landscape and looks ahead to the coming year, including where we see select opportunities emerging, as well as variation between the two markets. We conclude with three broad strategic themes and recommended strategies where investors may consider deploying their capital.

Americas Head of Research and Strategy

Canada Head of Research and Strategy

The sheer size and complexity of the Asia Pacific region means real estate markets and investment opportunities are as diverse as the region itself.

In the final chapter of ISA Outlook 2024, we discuss this complexity and how China’s new economies – such as high-tech manufacturing and biotechnology – are growing rapidly and, after more than two decades, Japan is hoping to bid sayōnara to deflation. In other key parts of the region – Australia, Hong Kong, Singapore and South Korea – central banks are near the end of their rate-hiking campaigns in a bid to lower inflation which, as in the rest of the world, could lead to a rebound in transaction activity.

Asia Pacific Head of Research and Strategy

China Head of Research and Strategy

Senior Strategist, Asia Pacific Research and Strategy

Published every year since 1993, LaSalle’s annual ISA Outlook is designed to help our clients and partners navigate the year ahead. It brings together smart perspectives and investment ideas from our teams around the world, based on what we see across our more than 1,500 assets that span geographies, property types and risk profiles.

As always, we welcome your feedback. If you have any questions, comments or would like to learn more, please get in touch by using our Contact Us page.

London (November 7, 2023) – Related Argent and joint venture partner Invesco Real Estate have appointed the main contractor and secured the debt finance for the development of Brent Cross Town’s second Build-to-Rent (BtR) building, enabling construction of 286 new homes. Galliford Try will deliver the homes and over 17,000 square feet of amenity and retail space, while the £97 million debt financing is provided by LaSalle Investment Management, further building on the significant momentum at the £8 billion net zero park town in London.

The debt financing takes the form of a Green Loan, lending dedicated to sustainable projects, which is linked to the strong environmental credentials of the building. The building is designed to be supplied with very low carbon heating and cooling from the development’s electric district heating and cooling network, which is being delivered in partnership with Vattenfall. In addition, the building aims to deliver a measurable net gain in biodiversity and to minimise construction waste and embodied carbon through efficient off-site manufacturing. LaSalle Debt Investments’ green loan structures are compliant with the Loan Market Association’s green loan framework. The overall Brent Cross Town development is committed to reaching net zero by 2030.

The announcement demonstrates the significant progress being made at Brent Cross Town. Six buildings are now underway, the first of which will be completed from the end of 2024. In total, over 930 homes, including affordable, market sale and BtR homes are on-site along with 662 student rooms in partnership with Fusion Students. Sheffield Hallam University will open its first satellite campus outside of Yorkshire at Brent Cross Town, and a joint venture between Audley Group and Senior Living Investment Partners (Octopus Real Estate and Pension Investment Corporation) will create a retirement village with around 150 homes.

Brent Cross Town is being delivered in partnership between Related Argent and Barnet Council and will create a total of 6,700 new homes, 3 million square feet of offices, a high street and schools surrounded by 50 acres of parks and playing fields including the new 4.5-acre Claremont Park which was completed last year. The new town will benefit from Brent Cross West station, which will be the first major new mainline station in London in more than a decade when it opens later this year, connecting with King’s Cross St Pancras in as little as 12 minutes.

The new contractor appointment and financing is part of the joint venture between Related Argent and Invesco Real Estate, the global real estate investment manager, formed at the end of 2022 to deliver £600 million of Gross Development Value, including over 800 homes as well as retail by 2025.

Galliford Try, one of the UK’s leading construction groups, is already delivering the first BtR building at Brent Cross Town. Its appointment by the Related Argent and Invesco Real Estate joint venture to deliver the second BtR building comprising 286 homes, a mix of market and discount market rent homes, will bring the total number of BtR homes under construction at Brent Cross Town to 535.

All will be developed and managed by Related Argent, which has just opened a brand-new premium rental development, Author King’s Cross on the King’s Cross estate. Related Argent’s BtR portfolio draws on the established record of Related Companies, which has over 71,000 homes across the United States. Known for its outstanding customer service, Related Companies has decades of proven experience in the sector.

The 286 new homes are designed by Allies & Morrison, with interiors by Conran and Partners, and range from studio to three-bedroom apartments, with block amenities shared with the first BtR building at Brent Cross Town, including a large central lobby with 24-hour concierge, wellness hub, including a gym, fitness studios, 25 meter pool and sauna, work from home spaces, private dining spaces, roof top terraces, podium gardens, guest suites and a cinema.

Tom Goodall, Managing Director of Related Argent, said: “There is strong momentum behind our BtR portfolio with our first rental homes now completed at Author King’s Cross and over 1,000 BtR homes under construction. Our joint venture with Invesco Real Estate at Brent Cross Town and the financing from LaSalle Investment Management is helping meet an increasing gap in the market and addressing the city’s growing demand for high-quality rental properties in vibrant places.”

John German, Managing Director, Residential Investments at Invesco Real Estate, said: “When Invesco and Related Argent closed our Joint Venture in October 2022, we only had one build contract and one loan in place. 12 months later, we now have secured all four build contracts and the necessary loan facilities to enable the project to move forward as we had planned. We are delighted that the Project Team achieved this key milestone which now allows the project to move forward into the delivery stage to enable these assets to be delivered into our investor’s existing BtR Portfolio of just under 1,100 units.”

Robert Fay, Director, Debt Investments at LaSalle Investment Management added: “We are very pleased to work with Related Argent and Invesco Real Estate to provide the debt financing for this project, which brings together market leaders in urban regeneration and best-in-class accommodation in a great location with strong transport links to Central London. The living sector is one of LaSalle’s highest convictions across our European lending and equity strategies. This financing is LaSalle’s 26th development loan made since 2012 and builds on our development lending track record, providing flexible, sustainable loans to high-quality sponsors.”

Bill Hocking, Chief Executive of Galliford Try, said: “We are delighted to be working once again with Related Argent on one of the most significant Build to Rent schemes in London. Our business has a strong track record in producing high-quality residential developments with the sector remaining a key focus for our Building business within our Sustainable Growth Strategy.”

Councillor Ross Houston, Deputy Leader of Barnet Council and Cabinet Member for Homes and Regeneration, said: “Barnet’s new park town has been carefully designed to meet the needs of our residents now and in the future with a range of options including social housing, private sale homes, student accommodation and homes built to rent. I welcome the progress being made on Brent Cross Town’s first new homes that are being built specifically with Barnet renters in mind.”

The BtR offering at Brent Cross Town forms a major part of Related Argent’s portfolio of over 3,000 rental homes alongside King’s Cross and Tottenham Hale. The first residents moved into its first BtR development, Author King’s Cross, in October 2023. Related Argent has plans to expand its rental portfolio beyond the 3,000 homes.

Ends

About LaSalle Investment Management | Investing Today. For Tomorrow.

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, LaSalle manages approximately $78 billion of assets in private and public real estate property and debt investments as of Q1 2023. LaSalle’s diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. LaSalle sponsors a complete range of investment vehicles, including separate accounts, open- and closed-end funds, public securities and entity-level investments. For more information, please visit www.lasalle.com, and LinkedIn.

About LaSalle Debt Investments

LaSalle Debt Investments is part of LaSalle’s growing $10bn Debt & Value-Add Strategies platform in Europe and invests in a diverse range of real estate credit products – spanning senior loans, whole loans, mezzanine, development finance, corporate finance, NAV facilities and preferred equity – with significant experience across various sectors, geographies, deal sizes and capital structures. Since launching the business line in 2010, LaSalle has been one of Europe’s most active alternative real estate debt providers with a long track record of lending to best-in-class sponsors.

About Related Argent

In 2015, Argent and Related joined forces to create an unrivalled UK property business and urban regeneration specialist. The company brings together the expertise and track record of Argent – the developer behind some of Britain’s most successful mixed-use places, and Related – one of the most innovative and prolific real estate companies in the US. The combined experience delivering ground-breaking projects such as King’s Cross in London, Hudson Yards and Deutsche Bank Center in New York, Brindleyplace in Birmingham, The Square in West Palm Beach, Florida and The Grand LA in Los Angeles is brought to bear on each of the projects.

Related Argent operates across a range of property sectors including residential, workspace, education, shopping, hospitality and leisure. Its work goes beyond bricks and mortar development. It also specialises in the services, facilities and experiences that are so important to urban life – art, culture, events, schools, skills & training programmes and renewable energy networks.

Related Argent is one of the UK’s leading developer-owner-operators and, since its inception eight years ago, has rapidly grown a £9Bn+, 12m sq ft mixed-use development pipeline. This includes major regeneration projects in London, at Brent Cross Town and Tottenham Hale, as well as a Build-to-Rent (BtR) scheme at King’s Cross, known as ‘Author King’s Cross’. It’s accessing global capital markets to deliver major new projects across the UK and is seeking to expand its BtR housing portfolio. On 1 May 2024, Argent will transfer all employees, projects and assets to Related Argent Limited.

Related Argent’s vision is to be a great city builder – for people, planet, and prosperity and its purpose is to improve urban life for all, everyday. This means developing for the long term – astutely, sustainably and with a sense of social purpose. Related Argent is delivering the places, homes, workspace, public space, arts, culture, events and services that our UK cities and town centres need. www.argentllp.co.uk

About Invesco Real Estate

Invesco Real Estate is a global leader in the real estate investment management business with USD 91.1 billion in real estate assets under management, 586 employees and 21 regional offices across the U.S., Europe and Asia. Invesco Real Estate has a 40-year investment history and has been actively investing across the risk-return spectrum, from core to opportunistic, in equity and debt real estate strategies, and in direct and listed real estate for its c.500 institutional client relationships during this time. In Europe, Invesco Real Estate has eight offices in London, Munich, Milan, Madrid, Paris, Prague, Luxembourg and Warsaw, and 191 employees. It manages 200 assets across 14 European countries and with assets under management of USD 18 billion. Source: Invesco Real Estate as at 31 March 2023.

About Galliford Try

Galliford Try is a trading name of Galliford Try Holdings plc, a leading UK construction group listed on the London Stock Exchange. Operating as Galliford Try and Morrison Construction, the group carries out building and infrastructure projects with clients in the public, private and regulated sectors across the UK.

About Brent Cross Town

Brent Cross Town is the neighbourhood at the heart of the Brent Cross Cricklewood regeneration programme. It is a joint venture between Related Argent and Barnet Council to develop a large-scale mixed-use development including new homes, retail and office space, as well as improved schools and greenspaces in the area. Early work started on site in early 2020 and construction is also underway on the new Brent Cross West station which is due to open later this year. Building on the strengths of this diverse part of the city, Brent Cross Town will draw inspiration from the best of London’s long-established neighbourhoods with all their complexity and character.

At its heart, will be a focus on sport, play, health and well-being. The new neighbourhood will provide 6,700 homes, state-of-the-art workspace for over 25,000 people, and pedestrian friendly streets and squares with local shops and restaurants that will complement the offer at Brent Cross Shopping Centre. The community will be supported by first-class public transport infrastructure, a new and improved network of walking and cycle routes and a series of new parks and other amenities. www.brentcrosstown.co.uk @brentcrosstown

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

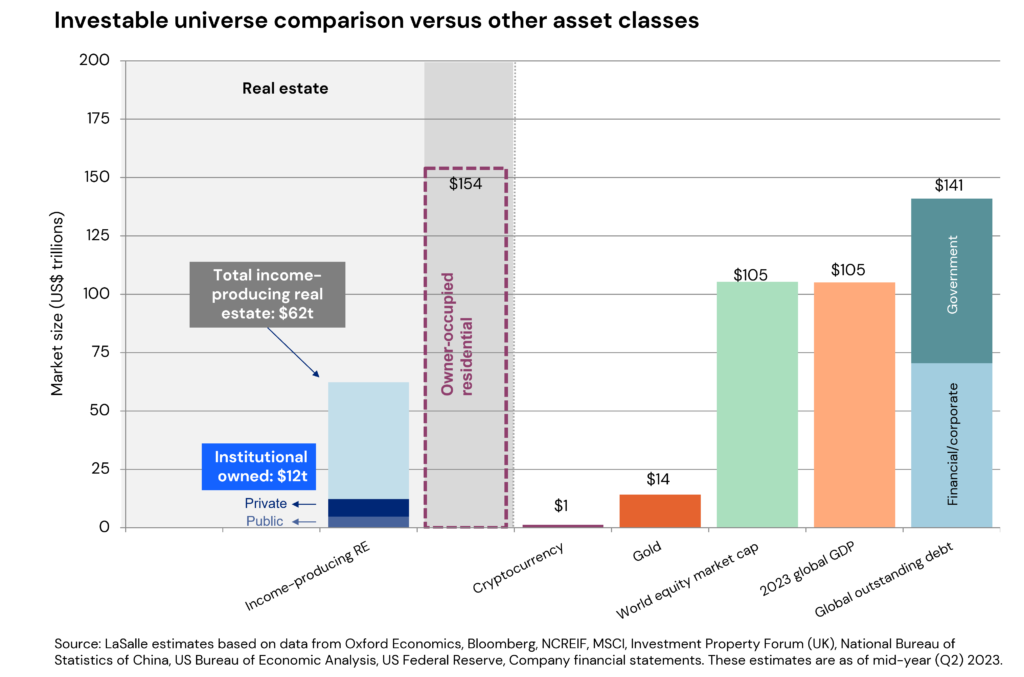

In an uncertain market, it is tempting to prioritize cyclical questions such as the risk of recession and the path of interest rates over structural topics with longer-run implications. But challenging periods in real estate markets can also be attractive times to build exposure to the asset class.1 Questions about how to build portfolios do not diminish in importance just because bond market volatility makes front-page news. In our view, one of the most useful starting points for approaching portfolio construction is having a sense of the size of the real estate investable universe and its subcomponents. This is why we regularly update our estimates of the real estate investable universe and have done so consistently since 2005.

We first shared our latest estimates for the size of the global real estate universe in the 2023 edition of ISA Portfolio View. As described there, the vast scale of real estate as an asset class is among the key pillars supporting the case for including property in multi-asset portfolio. But putting a thoughtful number on the size of the asset class is easier said than done. We believe it is worth the effort because quantifying the size and distribution of the market — rather than just a subset covered by a particular index or data source — helps investors sharpen their thinking on target allocations by asset class, geography and investment structure. A full description of our methodology, data sources and summary table by country is available here, and we are glad to provide additional detail upon request.

We estimate market size, defined as aggregate gross asset value, for three nested segments, shown below. The largest and most comprehensive estimate is for all property held for the income it provides, inclusive of all types of owners (except owner-occupiers) and all quality levels. Using a separate methodology, we also estimate real estate owned by institutional investors, and by one particular type of institutional investor — those whose equity is publicly traded.

Our analysis shows that one fifth of global real estate is owned by institutional investors, and 40% of that institutional ownership is by listed companies. The estimates also break down market size by country, property type and city, using a methodology combining several bottom-up and top-down sources.

We take a closer look in this ISA Briefing at three key findings from the real estate universe analysis: (1) global income-producing real estate has recently ebbed to a below-average size relative to GDP, (2) real estate value has a fairly even distribution across the three major global regions and (3) those regions differ significantly in how real estate is distributed across metros, implying different optimal diversification strategies.

Figures in trillions can be so enormous that they lose some meaning — so it is helpful to put those numbers in context. An illuminating comparison is to put income producing real estate alongside other asset classes like stocks and bonds, as shown in the graph below.

These estimates show global real estate is a smaller sibling to stocks and bonds but very much in the same family of major asset classes. Notably, owner-occupied residential real estate, which is not included in LaSalle’s real estate estimates, is significantly larger in size than all income-producing property, and even larger than the global fixed-income market.

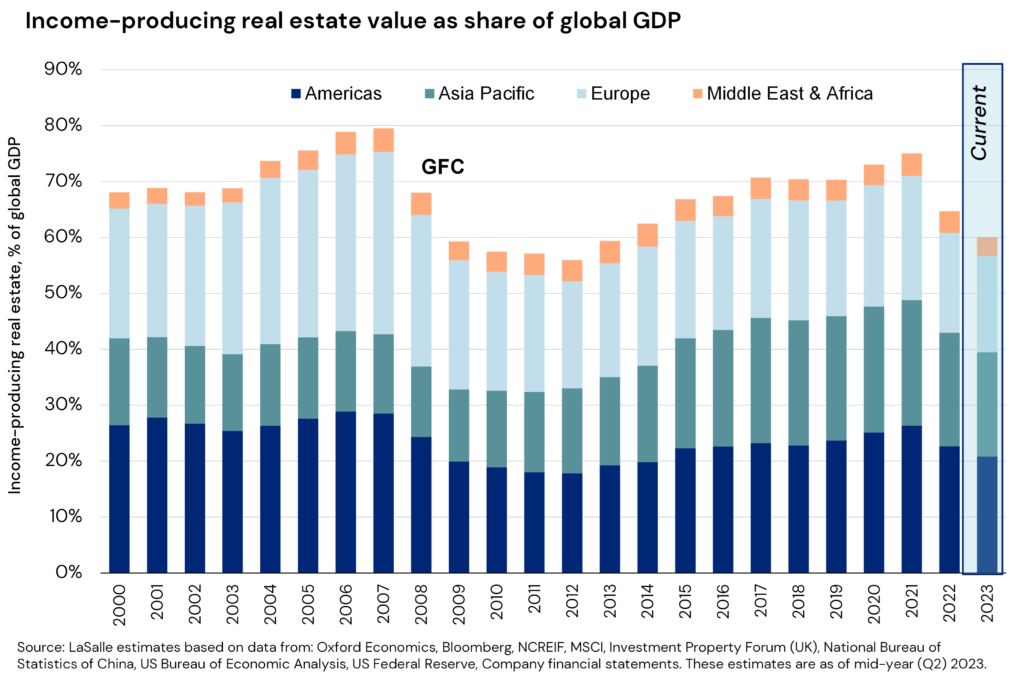

Another useful comparator, shown below, is against global GDP. We estimate that real estate is equal to 60% of global GDP in 2023. This puts it at a low ebb relative to recent history. This is consistent with the historic pattern of real estate comprising a higher share of GDP late in expansions and then a lower share of GDP in repricing episodes. Currently our real estate market size estimate is near previous cyclical lows as a share of GDP seen in 2009-2012. Since 2000, our real estate market size estimates have averaged 68% of global GDP.

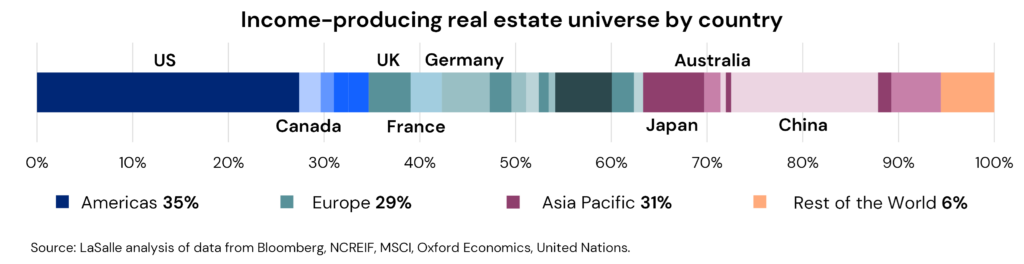

A second key finding from LaSalle’s universe estimates is the relatively even split in value observed between the three major regions of the Americas, Asia Pacific, and Europe. We estimate that 35% of income producing property is in the Americas, 31% in Asia Pacific, and 29% is in Europe. We believe these estimates from LaSalle’s real estate universe analysis better reflect the true opportunity set than other splits based on simple GDP or real estate indices, which can sometimes be lopsided based on where coverage is greatest or which types of investment fund products predominate. For example, 67% of the MSCI Global Property Fund Annual Index AUM is in North America.2

The split above suggests an even distribution of opportunities by region. At the same time, our national estimates also show global diversification can be achieved with a small number of countries. The eight countries with the most institutional-invested real estate together account for 70% of the invested universe. A focus on these larger countries — as well as multi-country funds — can enable investors to efficiently achieve diverse exposures, while also managing the challenges that come with differences in market practices, currency, regulation and building market knowledge.

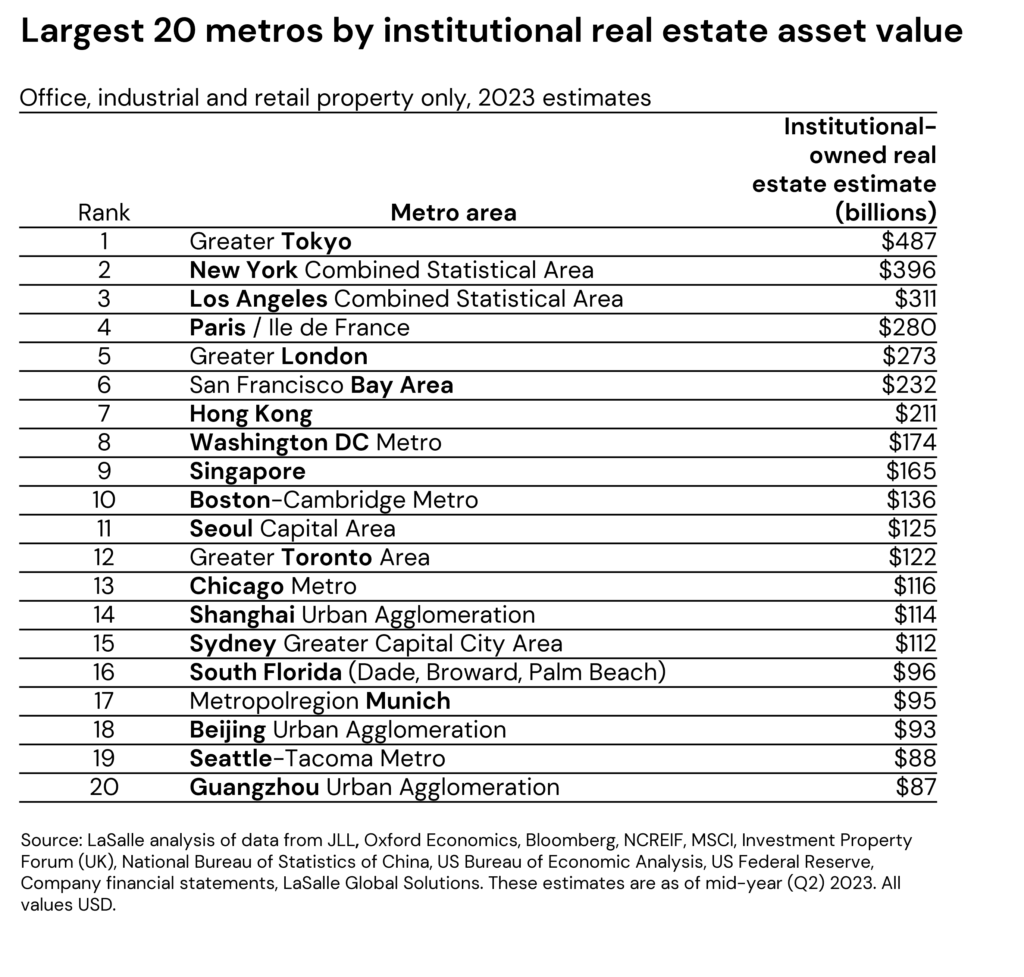

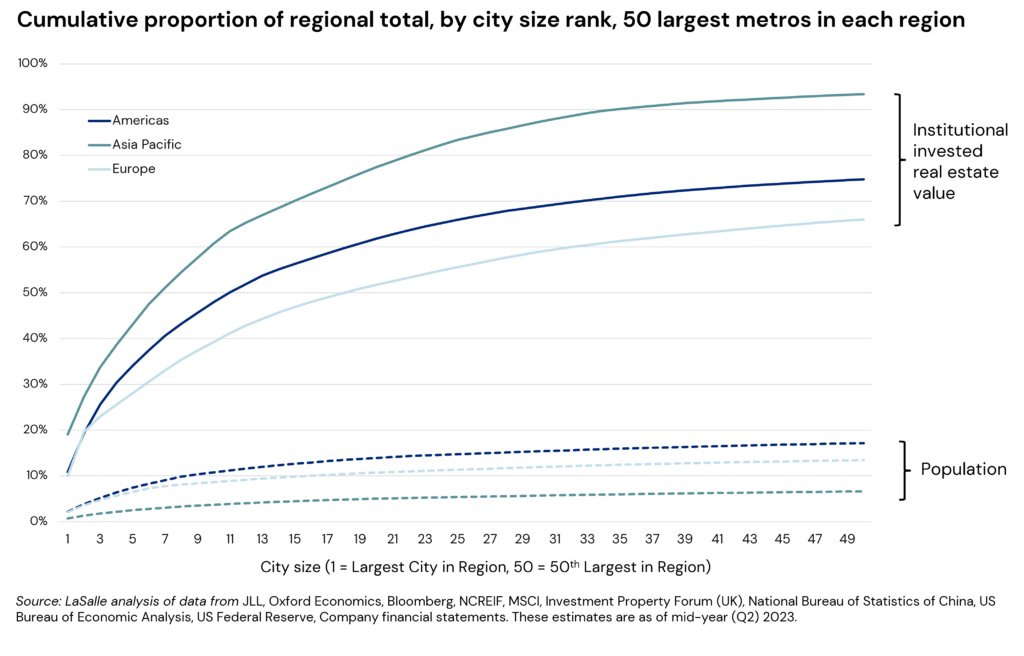

Our third notable finding emerges when zooming in one level further from the national level to individual cities. Cities and their surrounding metropolitan areas form the underlying building blocks of the real estate universe; they are often the basic level of analysis investors have in mind when comparing market allocations.

LaSalle estimates institutional real estate market size are for the entire metropolitan (metro) market — including the principal city and its suburbs that are economically connected to it, adopting official metropolitan area definitions from national statistical agencies where available.

Real estate held in institutional investor portfolios is highly concentrated in the largest metros, and these local market size estimates highlight the degree of that concentration. The 40 largest metropolitan real estate markets account for 58% of all institutional property. Some of the world’s largest metro areas dwarf many individual countries when it comes to institutional real estate ownership. Our latest estimates show that there is likely more institutional-owned real estate in Greater Tokyo than in all but three of the 201 countries covered in our estimates.

The metro market size distribution varies considerably across regions, with important implications for portfolio strategy. Institutional real estate ownership in Asia Pacific is more concentrated in its largest metros than in any other region. And its real estate is far more concentrated in a few cities than its population. In Asia Pacific, 18 metros account for 75% of institutional property, whereas the equivalent metro total is 52 in the Americas. In Europe, real estate is the most dispersed across cities, reflecting its more fragmented quilt of different jurisdictions. Over 100 European metros must be amalgamated to account for 75% of the regional total. Such dispersion makes the task of setting target markets even more complex, which is where tools like the recently released LaSalle European Cities Growth Index (ECGI) can help.

These differences impact investment strategy and approaches to diversification. Asia Pacific’s concentration of large institutional markets implies that investors may be able to achieve diversification by investing in fewer metros, but that it is also a region where each “bet” on geo-market allocation matters more. In Europe and North America, investors are more active across a larger number of medium-sized markets, offering diversification benefits as well as challenges in terms of access and efficiency.

Footnotes

1 Vintages around the time of market disruption tend to outperform, according to LaSalle analysis of data from the INREV Global IRR Index through Q4 2022. See page 30 of our ISA Portfolio View for a more complete discussion of this analysis.

2 Source: MSCI. Data as of 2022 (most recent available).

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.