-

LaSalle’s Eduardo Gorab, Chris Battista and Matt Sgrizzi discuss the outlook for REITs and ask if listed real estate is about to enter a new “golden era”? Listed real estate investment trusts (REITs) have faced a tough two and a half years, driven by the rapid tightening of financial conditions (see LaSalle Macro Quarterly, or LMQ, pg. 13). Sentiment towards REITs has been weighed down not only by the higher interest rate environment, but also by constrained bank lending, a barrage of negative headlines about commercial real estate and REIT underperformance relative to the broader equity market. But, as the saying goes, it’s often darkest before the dawn.

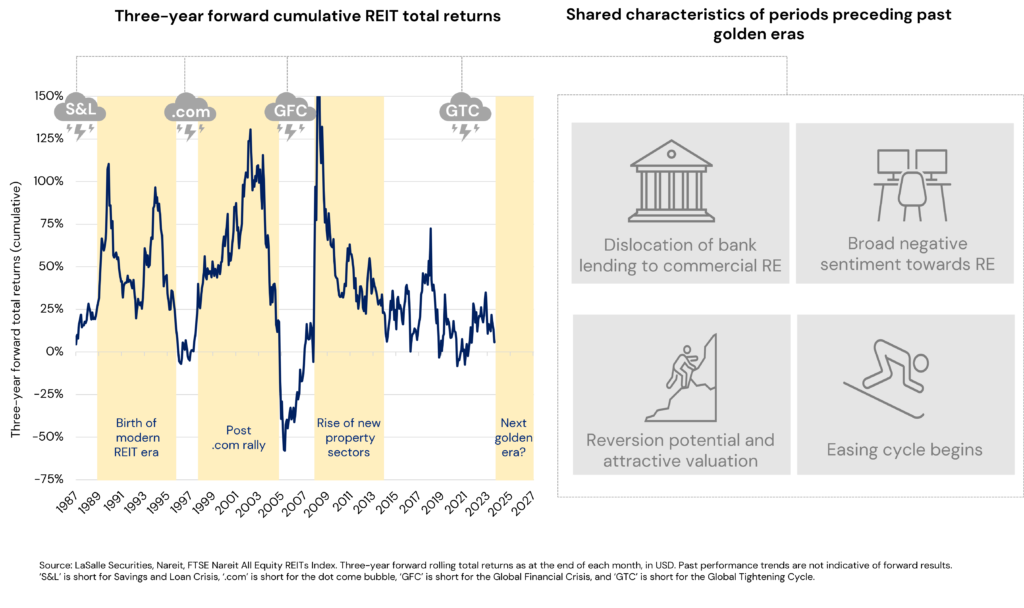

The modern REIT period has seen three “golden eras” of REIT investing (see chart below).1 These have been characterized by either a dramatic growth in the REIT market or outsized investment returns versus other asset classes, or both. The Savings and Loan (S&L) crisis spurred what is often considered the birth of the modern REIT era in the mid-1990s. During this period, the number of REITs increased by nearly 50%, while the market cap of that group grew nearly seven-fold. Following the Dot-com bubble, a period where REITs had been significantly out of favor, the REIT market endured a multi-year run of strong absolute performance in which it cumulatively outperformed broader equity markets by more than 300%. The period following the Global Financial Crisis (GFC) saw the rise of dynamic new property sectors in the public market, and another period of outperformance in which REITs led broader equities by 50%.

While each golden era was unique, our analysis finds that each period was preceded by challenging circumstances with four common elements (see LMQ pg. 14). These are:

- dislocation of bank lending to real estate;

- broad-based negative sentiment around real estate;

- underperformance versus broader equities which leads to attractive relative valuation and the potential for renewed outperformance; and

- an easing or reset of financial conditions, potentially aided by a central bank easing cycle.

Recent history, marked by a post-pandemic recovery followed swiftly by the Great Tightening Cycle (GTC), presents important similarities to these historical periods of severe market challenges. For instance, real estate bank lending is dislocated. An AI-driven tech frenzy and fears of a generalized “commercial” real estate malaise mean REITs have underperformed compared to equities (see LMQ pg. 22). Meanwhile, signs of an easing or stabilization in financial conditions and a potential global monetary easing cycle are becoming more apparent (see LMQ pgs. 9, 10 and 30).While history does not repeat itself, it does often rhyme. The presence of those elements in today’s market environment, and the potential for those concerns to flip to opportunities, may foretell the next REIT golden era. We discuss each of these factors in turn.

Challenged real estate lending represents an opportunity for REITs. The past two to three years have been characterized by a significant retrenchment in bank lending to real estate. According to the US Senior Loan Officer Survey (see LMQ pg. 16), the net balance between demand for loans and banks’ willingness to lend points to the widest undersupply of credit in the past ten years, except for during the depths of COVID-19. The shortage is evident in all styles of borrowing, from riskier construction loans to mortgages backed by traditional, defensive apartment assets.

This circumstance presents an opportunity for REITs given their strong financial positions and access to the capital markets. Having learned a painful lesson from the GFC, global REITs went into the GTC with their lowest leverage levels on record (see LMQ pg. 16), and nearly 90% of their debt on fixed rates and an average remaining term of seven years.2 Looking specifically at the US market, the overwhelming majority of REIT borrowing – nearly 80% – is from the unsecured market, at rates that are today almost 100 bps lower than a traditional mortgage. This relative advantage in both access and cost of capital positions REITs to potentially play the role of aggregator and to take market share.

“Commercial” real estate negativity is office-focused, but all real estate is not office. Headlines proclaiming the demise of commercial real estate usually involve a misleading generalization. Professionally managed, income-producing real estate generally should not be conflated with office specifically. It is well known that hybrid work and other factors have harmed office values. Office fundamentals are expected to remain relatively weak,3 with the sector’s growth outlook trailing nearly all other REITs globally. Office landlords will likely need to invest capital aggressively to maintain competitiveness.

These challenging office sector dynamics have unfairly cast a shadow over the broader real estate and REIT universe. In reality, office has over time become a smaller portion of the real estate landscape, especially in the public market; as of the date of this paper, only about 6% of global REITs by market capitalization are office focused (see LMQ pg. 20).4 The public market now offers a diverse sector menu comprising a wide range of dynamic sectors. These include industrial and logistics; forms of rental residential including multi- and single-family rental, manufactured housing and student housing; various formats of healthcare property; and exposure to tech-related real estate in the form of data centers and cell towers. Sectors other than office comprise the overwhelming majority of the public REIT market,5 and many of those sectors have growth outlooks that are forecast to produce earnings growth that is in line with or better than broader equities.6 That growth outlook is underpinned by a combination of secular demand drivers and declining supply levels, the other side of the higher interest rate coin.7

Media coverage naturally tends to focus on the national and trans-national arenas, but local political developments can be especially impactful for real estate investments. Such issues can fly under the radar, especially given many of the most relevant ones are only of interest to a specialist audience. For example, changes in policy around topics like the planning process, property taxes and transfer taxes (a.k.a. stamp duty) can have direct, measurable and immediate impacts on property cash flows and thus values. The distraction of the bright shiny lights of global geopolitics should not be allowed to excessively overshadow the critical local issues that impact real estate.

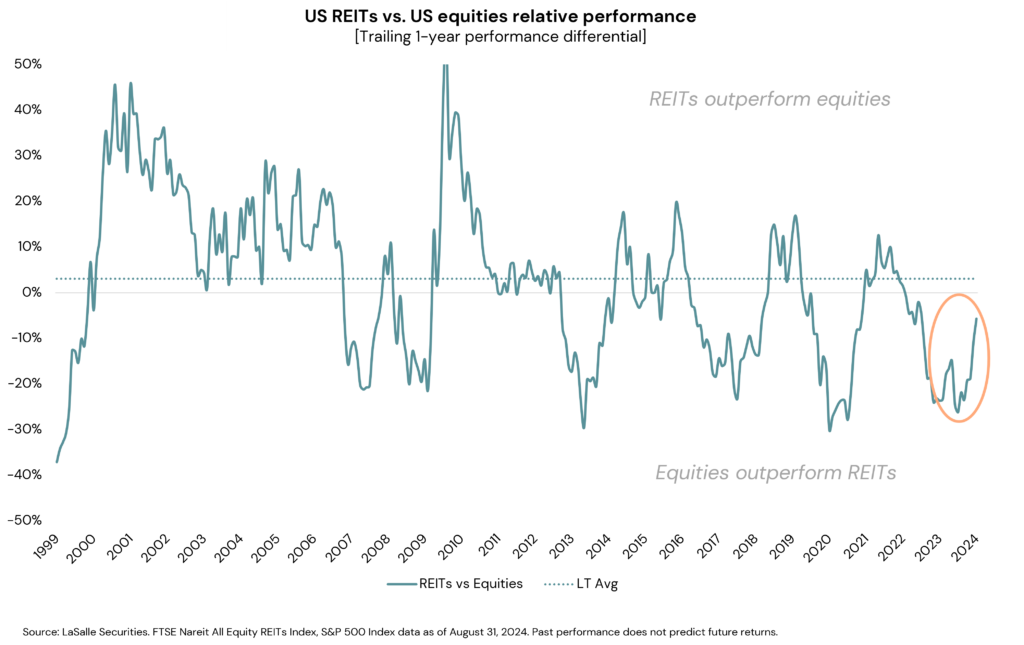

Underperformance may set the stage for a return to outperformance. The negativity around lending or financing concerns and the “death of office” have weighed on both the absolute and relative performance of REITs. The chart below shows the rolling one-year relative performance differential between REITs and equities; it indicates that REIT underperformance has reached its typical peak historical level before starting to reverse. Periods of underperformance have historically tended to reverse, and this instance is likely no different; indeed, the performance gap is already narrowing.

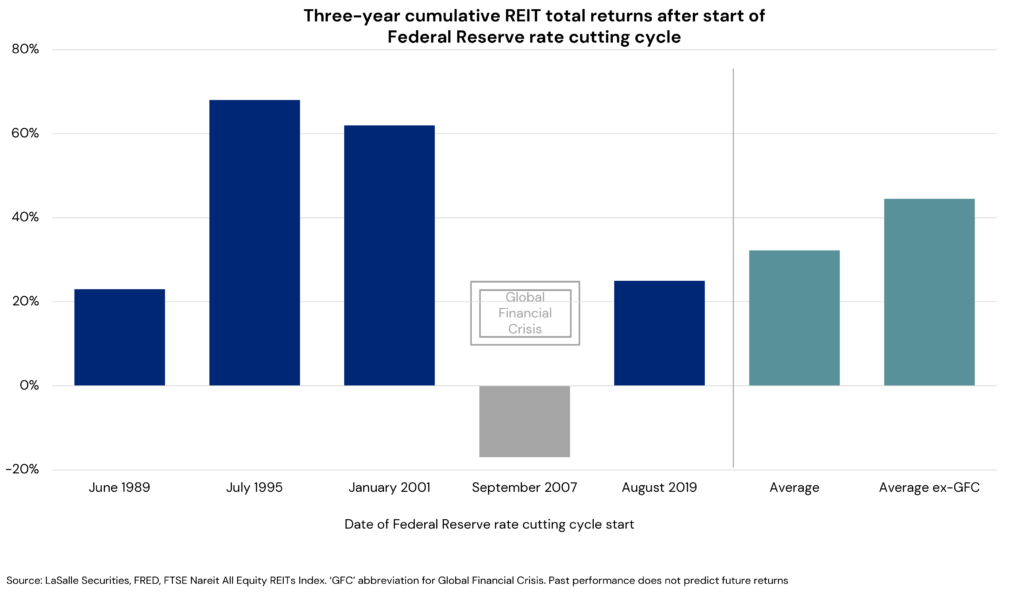

The start of a global monetary easing cycle. Real estate is a capital-intensive business that exhibits significant sensitivity to changes in financial conditions, an observation that holds for both directions of interest rate change. The downside of this dynamic was evident for much of 2022 and 2023, but the upside is likely coming into play. A global monetary easing cycle is now decidedly underway, heralded by the Fed’s 50 bps rate cut on September 18 (see LMQ pg. 31). REITs have generally performed well in periods leading up to and following a central bank easing cycle, as the chart below shows.

Over the past 25 years, REITs have produced total returns of 8% per annum, with 4-5 percentage points of that return coming from income. LaSalle’s base case underwriting for the next three years is for the REIT market to produce total returns of 9%, slightly above historical averages, with roughly four percentage points of that coming from income. That base case forecast incorporates today’s fundamental outlook and interest rate levels. Should any further easing in financial conditions occur, even only in the amount of 50 bps or 100 bps, those return expectations increase to 13% and 18% per annum, respectively, in line with previous “golden eras.”

LOOKING AHEAD >

- Pattern recognition is a useful approach that can help in predicting regime shifts in market conditions. Our study of historical periods of listed REIT under- and outperformance identifies a clear pattern. Namely, there are four common factors that have driven REIT strength after a period of challenges: dislocated bank finance, weak sentiment, underperformance versus broader equities, and the start of an easing in financial conditions.

- We also identify three historical “golden eras” for REITs — all of which were preceded by periods characterized by those four factors. These periods are those immediately in the wake of the S&L crisis, the Dot-com bust and the GFC.

- The current environment resembles the set up for these historical golden eras, suggesting that the REIT market may be on the cusp of its next golden era of investment, according to our analysis.

- Many of the factors supporting the REIT market’s upbeat prospects are also positives for real estate as a whole. For example, an easing in financial conditions has historically been a driver of strong forward REIT returns, as well as those for private equity real estate.

- That said, some of the dynamics are more specific to listed real estate markets. For example, REITs’ strong balance sheets and the cost of capital advantage of their unsecured borrowing options versus conventional mortgages positions listed players to seize opportunities.

Footnotes1 This analysis based on LaSalle Securities analysis of historical macroeconomic, capital market and listed market trends. Source for the REIT performance data cited below are the FTSE Nareit indices.

2 Source for debt pricing comments in this paragraph: S&P Global Market Intelligence, Green Street Advisors, company financial releases, company research and market analysis conducted by LaSalle Securities.

3 There is considerable global variation in office performance, and there are certainly exceptions to this generalization, especially in select Asia-Pacific markets and the higher end of the European office quality spectrum. For more discussion of global office trends, see our ISA Outlook 2024 Mid-Year Update.

4 Source: LaSalle Securities. Percent of companies classified as office focused within the global listed universe defined as the constituents of the S&P Developed REIT, FTSE EPRA Nareit Developed and Nareit All Equity Indices. Sector classifications determined by LaSalle Securities.

5 As measured by market capitalization. Source: LaSalle Securities. Global listed universe defined by the constituents of the S&P Developed REIT, FTSE EPRA Nareit Developed and Nareit All Equity Indices. Sector classifications determined by LaSalle Securities.

6 As based on LaSalle Securities proprietary modelling and consensus earnings forecasts for the Bloomberg World Index, a proxy for broader equity markets.

7 Higher interest rates mean development proformas use higher exit yield assumptions and more expensive development finance. When interest rates are high, all else being equal, the rents required to justify development are higher.

8 Based on proprietary internal LaSalle Investment Management modeling of securities returns. There is no guarantee that such forecasted returns, or any other returns referred afterwards, will materialize.This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

Jul 01, 2025

PERE: Q&A with Global CEO Mark Gabbay

LaSalle’s Global CEO sat down with PERE to discuss the world’s simplest, most complicated asset class.