-

A prudent person sees trouble coming and ducks.

A simpleton walks in blindly and is clobbered.

— Proverbs 22:3King Solomon’s words of wisdom have been passed down to us for 3,000 years. They still resonate, especially in this modern translation,1 even though the “trouble” is no longer invading Assyrians or Babylonians but the type of danger we bring on ourselves through an all-too-human combination of ingenuity, hubris and ignorance.

Watch any movie from the 1930s to the 1960s and you will see actors inhaling tobacco smoke with abandon. We know better now. Like the generational awareness of the harm caused by tobacco products, real estate owners have gradually become aware of the dangers lurking in certain building materials and contaminated soil. Starting in the 1960s, societies have spent fortunes cleaning up “miracle products.” Asbestos, PCBs, dry cleaning solvents, herbicides and lead pipes were all considered state-of-the-art technologies at various points in human history. None of these inventions were designed with the intention of killing people. They all started with a noble purpose – whether suppressing catastrophic fires, insulating transformers, cleaning wool suits or producing a pleasing nicotine buzz that also curbed the appetite. The “externalities” associated with societal damage from the use of these products took decades to discover and billions to eradicate.

Greenhouse gas emissions share a common ancestry with these miracle products. Heating buildings with diesel fuels, running gas lines through city streets, producing electricity with coal-fired plants—these were all logical, economical, and sensible solutions to the problem of bringing energy to homes, businesses and buildings of all types. The industrial revolution accelerated the growth of cities and raised the quality of life for millions of people by dragging them out of rural poverty. As we now know, society’s dependence on fossil fuels creates new problems which must be dealt with.

The recognition that miracle products can carry hidden (or not so hidden) dangers follows a predictable pattern. Here is what the step-by-step process often looks like:

Evidence and awareness. An environmental problem often requires decades of scientific study and mountains of evidence to convince people that a change is necessary. Even as this evidence accumulates, vested interests organize counterattacks to convince society that the problem is non-existent or over-stated. Eventually the harm to human life becomes so obvious that denial becomes a “fringe position.”

Market demand. In many cases, the process of partial “market adjustment” can begin ahead of government action. Voluntary data collection and industry-led reforms start the slow process of change. In the case of greenhouse gases, the marginal contribution of each emitter is so small, and so embedded in society, that government interventions sometimes lag market-led shifts (e.g., the adoption of LED lighting or heat pumps).

Regulatory response. Yet, government interventions are almost always needed to accelerate and complete behavioral change to truly eliminate harm to the environment and to human life created by “externalities.” These regulations and policy responses often get pushback as competing outcomes are debated in the political arena. Economists agree that putting a price on carbon would be the most efficient and effective solution, but a market mechanism for carbon pricing requires government intervention — in the form of a carbon “tax” or to set up an emissions trading scheme.

Benchmarks and best practices. Eventually, the rise of data benchmarks and peer group comparisons begins to shed light on who, where and how successful “treatments” are applied to any environmental problem. Engineering and laboratory science helps inform this stage of the process, as does public health or industry group data. Integration with market investment processes and decisions leads to a focus on reversing years of damage to the environment and compliance with new regulations and guidelines. At this stage, market-driven and regulatory-driven changes start to converge.

Price integration. Feedback loops are established where type 1 errors (false positives) and type 2 errors (false negative—or overlooked problems) are exposed.2 In loosely regulated situations like climate change, the efficient market hypothesis (EMH) takes hold as the change process gets partially or fully priced by consumers and producers. Economists and policy analysts favor the practice of placing a “price” on an externality to compensate society for the harm. In practice, though, compensatory payments to offset environmental damage are often decided through the courts and litigation.

Continued market and regulatory evolution. The enforcement of tighter regulations also follows its own trajectory depending on the governance structure of a particular country or urban jurisdiction and the toxicity of the problem. The discipline of epidemiology, using population data and public health analysis, is especially helpful at this stage of refining the policy solutions.

The Transition from “Data” to “Wisdom”

For the de-carbonization of buildings, various markets and countries are well into Step 3 (Regulatory Response) and Step 4 (Benchmarks and Best Practices). In Europe the “theory of change” is focused more on EU-wide or national policies to promote energy disclosures through top-down regulatory solutions. In the United States, the emphasis is based more on voluntary pledges, market solutions and regulations that are based on specific local jurisdictions. In most developed countries, steps 5 (Price Integration) and 6 (Market and Regulatory Evolution) are underway, but both have a long way to go.

The rise of real estate sustainability benchmarks (like GRESB) has accelerated in recent years. In many cases, they have expanded to include social factors and tenant well-being alongside environmental metrics. The next hurdle, though, is to establish materiality tests that infuse meaning, and determine financial impacts based on the volumes of reporting that the industry has started to produce and disclose.

Reading through ESG reports often reveals the triumph of reporting and public relations over salience or relevance. The conjoint challenges of reducing building emissions alongside improving the well-being of building users and the surrounding communities can be obscured by data denominated in less familiar metrics like tons of CO2 or Kilowatt hours. In time, and with experience, the emphasis will shift to what truly moves the needle on all elements of the “sustainable investing” paradigm—and which metrics give off misleading or meaningless “virtue” signals.

Financial metrics align most closely with the “fiduciary duty” of an investor. Moreover, stakeholders have decades of experience analyzing and interpreting financial data. It will take additional time and effort to convert environmental data into financial terms or to simply raise the consciousness of how to interpret energy and emission data in its own right. (LaSalle’s work on the “Value of Green” synthesizes studies of the evidence linking sustainability metrics and financial outcomes. An update on this work is below.)

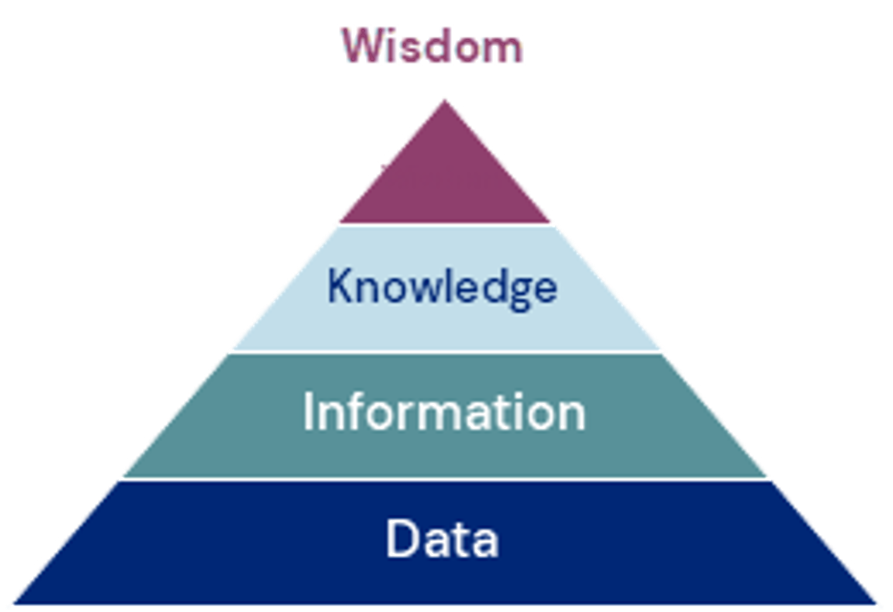

In writing Proverbs, King Solomon gathered centuries of wisdom based on experience. In the modern world, we often believe that the steps to wisdom are built on a foundation of knowledge, information, and data. The famous “DIKW” hierarchy has been a mainstay of information sciences since the 1930s. Sustainability wisdom is still in the process of being formulated and likely requires more time to make progress. Fortunately, the foundations of this wisdom are already being put in place—first through data (the modern way to refer to many, many experiences), then information (organized and analyzed data), eventually leading to knowledge (patterns are identified and the “what” and “why” questions are answered) and finally reaching the status of accumulated wisdom (how to respond). This is a path that humans have traveled before. More lives are at stake this time around and the wisdom may not be easily agreed upon by all industries, countries and stakeholders. Nevertheless, the search for sustainability wisdom must continue and time is of the essence.

Revisiting LaSalle’s “Value of Green”

In September 2023, LaSalle published our ISA Focus report What is the value of green? Looking at the evidence linking sustainability and real estate outcomes. The report presents a framework on how sustainable attributes of properties can be viewed as both as drivers and protectors of value, along with showcasing findings from the broader literature. We continue to maintain a Value of Green tracker, monitoring research on this subject as it is produced. Some of the findings that have surfaced since the release of our initial report are worth highlighting:

- In early 2024, CBRE reported in their UK sustainability index that efficient properties outperformed inefficient properties by close to 2% per year in terms of total return, over the course of 2023 across three major property types. The efficiency of buildings was delineated through EPC ratings.

- UBS reported in late 2023 that a green premium of 28% and 19% in price per square foot was in evidence in the New York and London office markets, respectively, when comparing office transactions based on LEED/BREEAM certifications. This premium was also established in cap rates, showing a 36 and 27 bps premium for New York and London respectively.

- MSCI published a report on price premiums for green buildings, and how they have changed over time. Looking at offices in Paris and London, a clear trend emerged from 2019 onwards showing a growing sale-price gap between offices with and without sustainability ratings. In the case of London, the gap was close to non-existent before 2019 and had since grown to 25% as of the latest reported data point in late 2022.

Beyond the direct links between sustainability and historical investment performance in terms of return, rent and value premiums, more signals are emerging as available data on the topic grows, and becomes increasingly forward looking:

- In 2024, JLL published in their “Green Tipping Point“ report on how the supply/demand balance is shifting in favour of sustainable offices across the globe, as tenant demand evolves. JLL projects a 70% unmet demand across 21 global office markets.

Beyond results based on backward-looking data, detailed case studies of investments into sustainable initiatives are being published. The JLL report “Future-Proof Your Investments“ showcased opportunities for sustainable New York offices; another example is CBRE’s report “The impact of on-site rooftop solar on logistics property values.”

Tobias Lindqvist

Strategist, Climate and Carbon Lead, London

Sources:

CBRE (March 2024) UK Sustainability Index Results to Q4 2023. CBRE

P. Torres, G. Bolino, P. Stepan (2024) The Green Tipping Point. JLL

T.Leahy (2022) London and Paris Offices: Green Premium Emerges. MSCI

P. Torres, J. del Alamo (July 2024) Future-proof your investments. JLL

D. Marina, J. Tromp, T. Vezyridis, O. Bruusgaard (July 2023) The impact of on-site rooftop solar PV on logistics property values. CBRE

O. Muir, Y. Chen, T. Metcalf et.al (Dec 2023) Green premium: Study of New York and London Real Estate finds strong evidence for a ‘green premium’. UBSWhat can we learn from simulations?

The de-carbonization of buildings is taking place in a complex and ever-changing environment. It is a multi-dimensional problem replete with uncertain outcomes, regulatory change, shifting societal norms and markets, and the politicization of sensitive issues.

At the June 2024 MIT World Real Estate Forum, Professor Roberto Rigobon unveiled a “sustainability simulation” game patterned on his pathbreaking work on social preferences for the European Commission. The technique shows how the traditional economic conceit that we make “resource trade-offs” does not accurately capture how humans make decisions when faced with multi-dimensional choices.

In the simulation, the audience was given nine choices for different retrofit projects for a commercial building. Each choice resulted in simultaneous movement across three metrics that the audience had already established that they cared about — changes in NOI (profitability), CO2 emissions, and tenant satisfaction/well-being. The cost of the projects was amortized into the NOI calculations and the other metrics were also calibrated based on actual data from the US.

The simulation showed that a knowledgeable real estate audience rarely solves just for “pure profits” at the expense of tenant well-being or CO2 emissions. The simulation also mimicked reality—where sometimes profitability moves in synch with reduced CO2 emissions and other times it moves it moves in the opposite direction. The simulation was designed to show how the co-movement depends on the local market and the type of de-carbonization project. Tenant well-being and CO2 emissions could be implicitly linked to revenue when and if participants believe that occupancy, rents and capital raising are all interconnected.

Through their choices, the audience tried to optimize across all three priorities at once — leading to an interesting result that revealed their average willingness to “pay” to reduce a ton of CO2 emissions of about $200 ton. Yet, if asked directly how much they would pay to reduce a ton of greenhouse gas coming from a building, it seems unlikely that many would have volunteered to pay that much. This finding also shows how the language of profitability and returns is much more advanced than the metrics and concepts associated with either decarbonization or tenant satisfaction. And that all these metrics are linked, but not fully integrated in the minds of real estate professionals.

Only a few participants in the game focused only on reducing CO2 (at the expense of decent profits). And just a few focused exclusively on profitability at the expense of tenant satisfaction or CO2 emissions. This seems like a reasonable facsimile of what enlightened investors will do — especially when they know that their actions are being disclosed. As we learn more from these simulations, it is possible that policy makers will be able to refine the mix of incentives and regulations that govern the real estate industry.

Jacques Gordon

Cambridge, MassachusettsLOOKING AHEAD >

- As we advance through the six stages of market wisdom, sustainable features in real estate move away from purely “virtuous” and toward increasingly meaningful drivers of investment value. As noted in our ”Value of Green” report the challenge for investors is understanding where, when and how sustainability is driving performance, which is highly variable across markets and sectors. Given LaSalle’s global reach, we are well positioned to observe, learn and act to enhance and protect asset values for our clients, and gain and share wisdom in the process.

- Markets are shifting towards wider alignment with a more sustainable future, new data and findings are continuously published. At LaSalle we also focus on the data generated within our walls, linking our own initiatives driving sustainability with their associated investment outcomes, bringing our own data and experience into the DIKW hierarchy.

- Recognizing the importance of meaningful benchmarks to drive decision-making (Stage 4), LaSalle has been leading an industry initiative to develop an improved solution for decarbonization pathways in the US and Canada, which could be adopted by CRREM and others globally. More meaningful decarbonization pathways will help investors properly measure transition risks and set targets, setting the industry up to make real progress in decarbonizing the built environment.

- Evolution over the Six Stages will likely be uneven over time, geography and investor type. This unevenness could provide investors at more advanced stages an advantage over less progressed investors. For instance, an investor who has incorporated a carbon business case into their investment process is at an advantage to appropriately price opportunities. For example, it should help investors identify attractive brown-to-green strategies.

Footnotes1 The Message, translated from the Hebrew scriptures by Eugene Peterson (1993-2002).

2 These are all part of the learning that occurs with any “treatment hypothesis.” The science of public health provides solid evidence to weigh whether the “treatment” is helping, hurting or having no impact on the eradication of the underlying disease. In real estate, a good example of this is the gradual discovery that with certain types of asbestos, it is more dangerous to remove it than to “encapsulate” it in an existing structure. The science of “decarbonization” is still being established to determine whether, for example, the mass production of lithium batteries does as much harm as the burning of fossil fuels. For real estate and climate change, the “treatment” will likely focus on energy efficiency/ decarbonization interventions that are a combination of government penalties/incentives and voluntary actions. The effectiveness of these treatments will depend on compliance, market response, and how well interventions find acceptance through the political process.

Important Notice and DisclaimerThis publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

Dec 02, 2024

PERE: Sustainable investing

Ryu Konishi and Julie Manning spoke to PERE about the growing importance of sustainability as part of investment decision-making and creating a net zero carbon pathway.