-

The COVID-19 epidemic has grown more severe by several orders of magnitude over the past month.

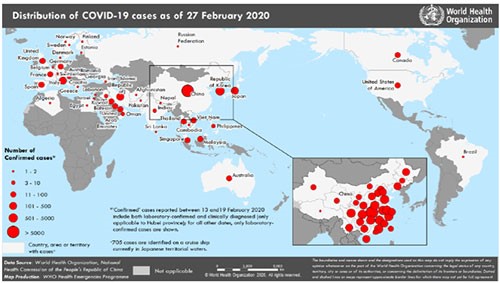

With more than 84,000 cases globally[1] ,it is now ten times larger than the SARS epidemic and has spread beyond China to more than 50 other countries. New cases have declined in recent days within China, but they have accelerated across the rest of the world. As the Chinese government and international health organizations on the front line have made clear, this global healthcare crisis is still growing, and the risks of underreacting are greater than the risks of overreacting.

The swift actions of courageous health care providers and the everyday sacrifices of people across Asia have helped to buy time for the rest of the world to be better prepared for the arrival of COVID-19 in their own countries.

In the highly interconnected society and economy of 2020, postponed travel, working from home rather than the office, and canceled in-person meetings and conferences are a small price for reducing the risk of a life-threatening, and still not fully understood, illness. For many across the Asia-Pacific region, the burden of containment has gone far beyond these inconveniences. Millions of households are experiencing economic hardship, coping with family separation, and enduring restricted freedom of movement in their own communities – all this before the toll of human suffering from the disease itself is taken into account. The swift actions of courageous health care providers and the everyday sacrifices of people across Asia have helped to buy time for the rest of the world to be better prepared for the arrival of COVID-19 in their own countries.

Economic impacts seem like a secondary concern at a time like this, but they are highly relevant for government leaders, policy makers, and investors who must first get through “crisis management” and then begin to make plans for the future. In China, which is now gradually loosening the largest quarantine in human history, the crisis is a simultaneous demand and supply-side shock. Several forecasters put a high likelihood on Chinese GDP contracting in year-over-year terms in the first quarter. At the same time, the Chinese government has already unleashed stimulus packages intended to help get business going again and to keep the financial system operating smoothly – and more stimulus announcements are expected. The governments of Singapore, Hong Kong and South Korea have recently announced their own stimulus packages, and other counties in Asia are likely to do the same.

This month’s macro deck summarizes the impact of the COVID-19 epidemic on global economic forecasts and on financial market prices. Beyond temporarily lost output, interrupted supply chains, a sharp decline in travel and tourism, and declining consumer confidence, the ripple effects have just begun spreading from Asia to Europe and North America. Property investments in China have seen direct impacts in the form of halted work at construction sites and retail rent moratoriums. Similar effects are likely in other intensely affected markets from South Korea to Northern Italy. Yet this is also a time when the durability of real estate income streams is likely to distinguish property as a stabilizer relative to other asset classes, as most leases are likely to generate income despite these temporary shocks.

The COVID-19 crisis is evolving daily. Although the first case was diagnosed on the last day of 2019, the impact will be felt far beyond the first quarter of 2020. The tumultuous end of February 2020 will go down in economic history as the week when the financial markets finally woke up to the warnings of the World Health Organization. Risk assets like stocks and high-yield bonds have entered “correction” territory in many countries. As we have pointed out before, fear tends to be self-reinforcing in economic decision making as people adjust consumption and investment decisions and perceptions quickly become realty. It is unknown how quickly the virus will be contained worldwide. Likewise, the longer-term impact on economic growth and real estate markets is highly uncertain. LaSalle’s investment teams expect to address the concerns of our tenants and clients through rapid-response communications and business-continuity plans; these actions have already commenced across our China portfolios. Real estate investors can draw some comfort from the insulating effect of real estate’s long-term contractual income and from the heavier weight of capital seeking stabilized income-generating assets as risk-free interest rates fall to all-time lows in several markets.

[1] See the World Health Organization website for continual updates: https://go.lasalle.com/e/579181/2020-02-29/vdxnmf/898126978?h=iIsAuG6NtoLc1mNbzDxqAasaTIIcyr1uQQt-Jkmi-n8

Nov 11, 2024

ISA Briefing: The “Red Sweep” and real estate: has the outlook changed?

ISA Briefing, “The Red Sweep and real estate”, which provides our quick thoughts on what the election result means for real estate and investment strategy.